Automation · AI · Robotics — June 8, 2026

Robots: Valuations and The Scaling Question

Are We There Yet?

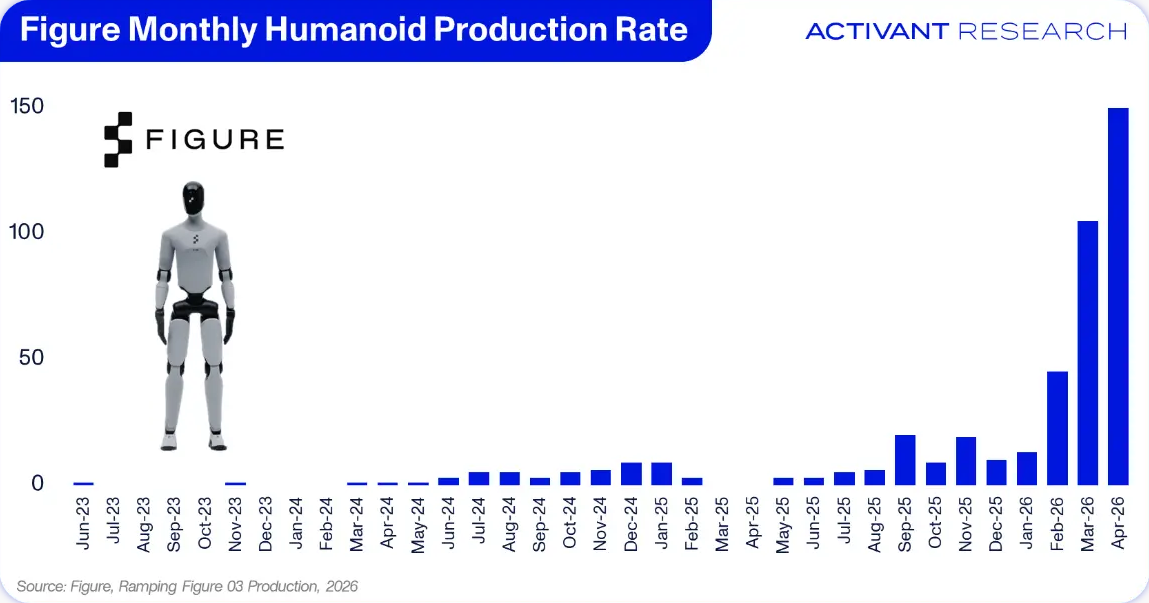

In early 2024, Goldman Sachs projected the total addressable market for humanoid robotics would reach $38 billion by 2035.1 Eighteen months later, Figure – a single humanoid company that had shipped a total of ~150 robots – raised a $1 billion Series C at a $39 billion post-money valuation. At the same time, FANUC, the world’s largest industrial robot manufacturer, with ~$5.5 billion in annual revenue and more than a million units installed globally, carried a market capitalization of ~$36 billion.2 That’s a pre-revenue startup valued higher than Goldman’s ten-year forecast for the entire market it operates in, and higher than the largest industrial robotics manufacturer in the world.

This may seem wild, but the rationale depends on the answer to a single question, one that everyone with an interest in robotics is trying to answer: can robotic intelligence scale the same way that language models did?

Robots: One of our Oldest Ambitions

The need for general purpose automation is clear. Today, there are 380,000 unfilled manufacturing jobs in the US, with 26% of the workforce already over 55. By 2035, the US is expected to face a manufacturing labor shortfall of around 2.7 million workers. Germany anticipates a gap of 7 million workers by the same year, and Japan faces 11 million by 2040, with a third of its population already over 65. China’s workforce peaked in 2017, and its working age population has been shrinking since 2011. These demographic realities are forcing businesses to shift from asking whether a robot is cheaper than a human worker to whether a robot can perform a job for which no human can be found.

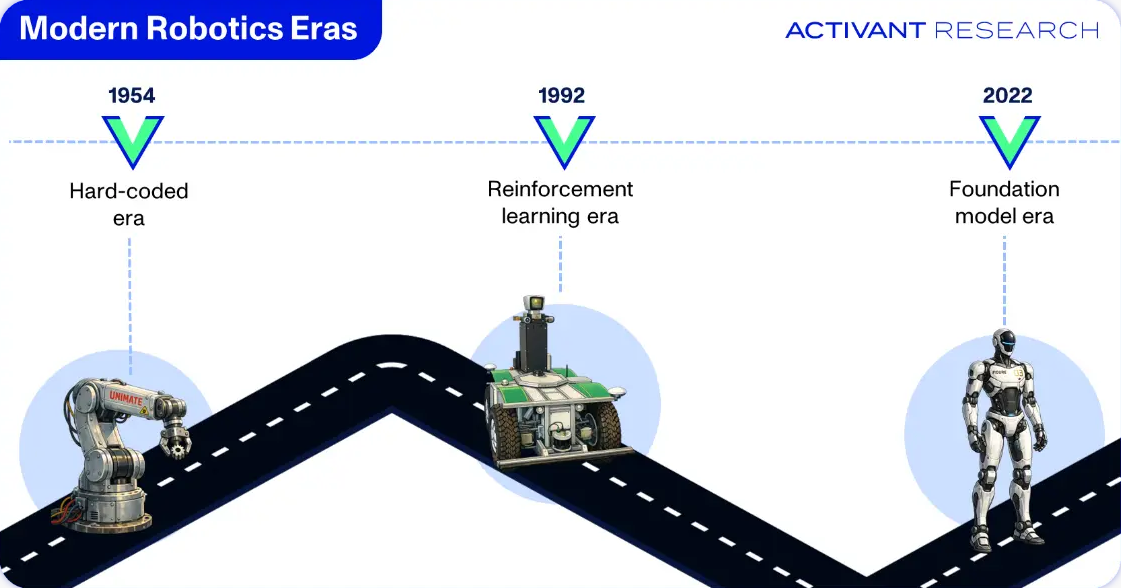

We’ve been trying to automate physical work since the Middle Ages. Al-Jazari first documented programmable automata in 1206, and Leonardo da Vinci sketched a mechanical knight sometime in the 15th century. The defining principle of modern robotics arrived in 1804, when Joseph Jacquard invented a loom controlled by punch cards, a machine capable of executing a stored program to automate physical work.345 When George Devol and Joseph Engelberger installed the first industrial robot, Unimate, at a General Motors plant in New Jersey in 1954, it was, at its core, a Jacquard loom for die casting: a programmable machine performing repetitive or dangerous tasks that humans would rather not do.6

For the next forty years, industrial automation was dominated by FANUC, Yaskawa, KUKA, and ABB, all of which built progressively more sophisticated and specialized solutions. Each robot was programmed for a single task, locked behind a safety cage, and required a full engineering effort for every new configuration or use-case.

Two developments broadened the market in the 2000s. Universal Robots (acquired by Teradyne in 2015 for $285 million) added force-sensing, removed the safety cage, and introduced cobots: robots designed to work alongside humans in industrial settings.7 Surgical robots then proved that the technology could extend beyond the factory floor. Intuitive Surgical’s da Vinci (FDA-cleared in 2000) gave surgeons near-unattainable precision, demonstrating that a robot’s value extends beyond labor replacement to enabling tasks that a human cannot perform as well alone.8

Despite decades of progress and clear demand, these robots remained largely confined to specialized use cases that offered high repeatability to support their need for single-task programming. Robotics never achieved the scale we demanded, because we never achieved general-purpose robotics.

Every previous robotics hype-cycle hit the same wall: machines could only execute tasks that they were explicitly programmed for. Cobots and surgical robots expanded where robots could operate and what they could achieve, but neither solved the fundamental problem of making robots learn. From Jacquard’s loom to the most advanced industrial arm of 2021, the process was the same: human programs, machine executes. Intelligence was still profoundly human.

This began to change in 2022.

Why It Might Work This Time

Is it finally possible for a robot to learn from demonstration, generalize to new situations, and improve with scale? There is increasing evidence to suggest it is – and if it is, everything about robot economics changes.

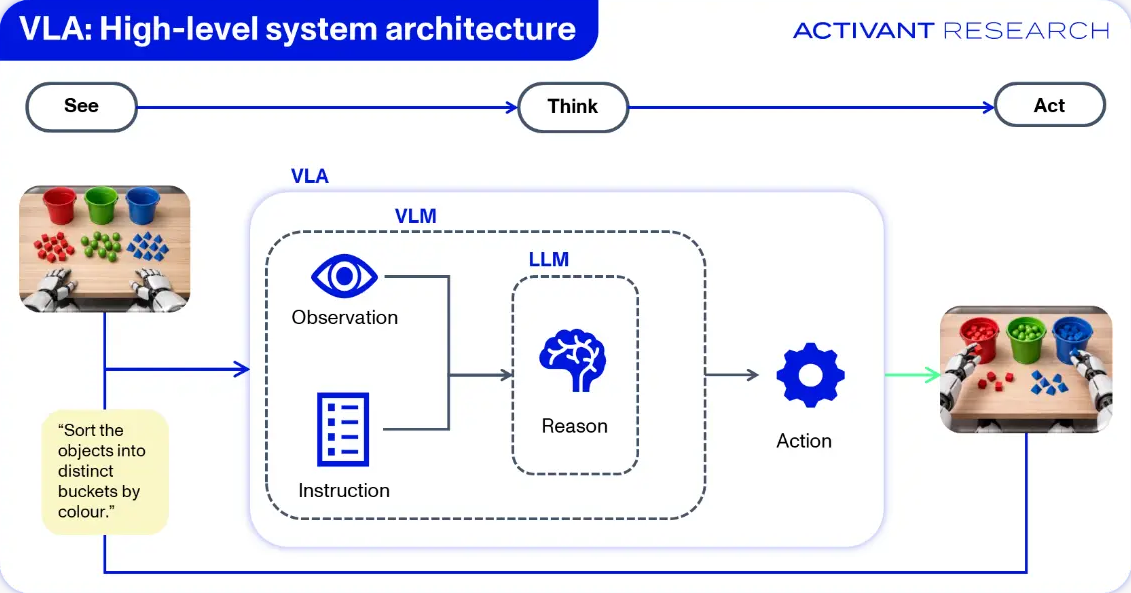

The VLA Revolution

Google DeepMind released RT-2 (Robotic Transformer 2) in mid-2023 and established the vision-language-action (VLA) paradigm.9 By fine-tuning a vision-language model (VLM) on robot demonstration data, the researchers effectively glued spatial understanding onto the “brain” of an LLM. Piggybacking on the intelligence gains made in LLMs, RT-2 achieved a 62% zero-shot manipulation task success rate (nearly double the performance of its predecessor, RT-1).10

For the first time, a robot could perform tasks it had never been explicitly trained on, using knowledge transferred from internet-scale pretraining.

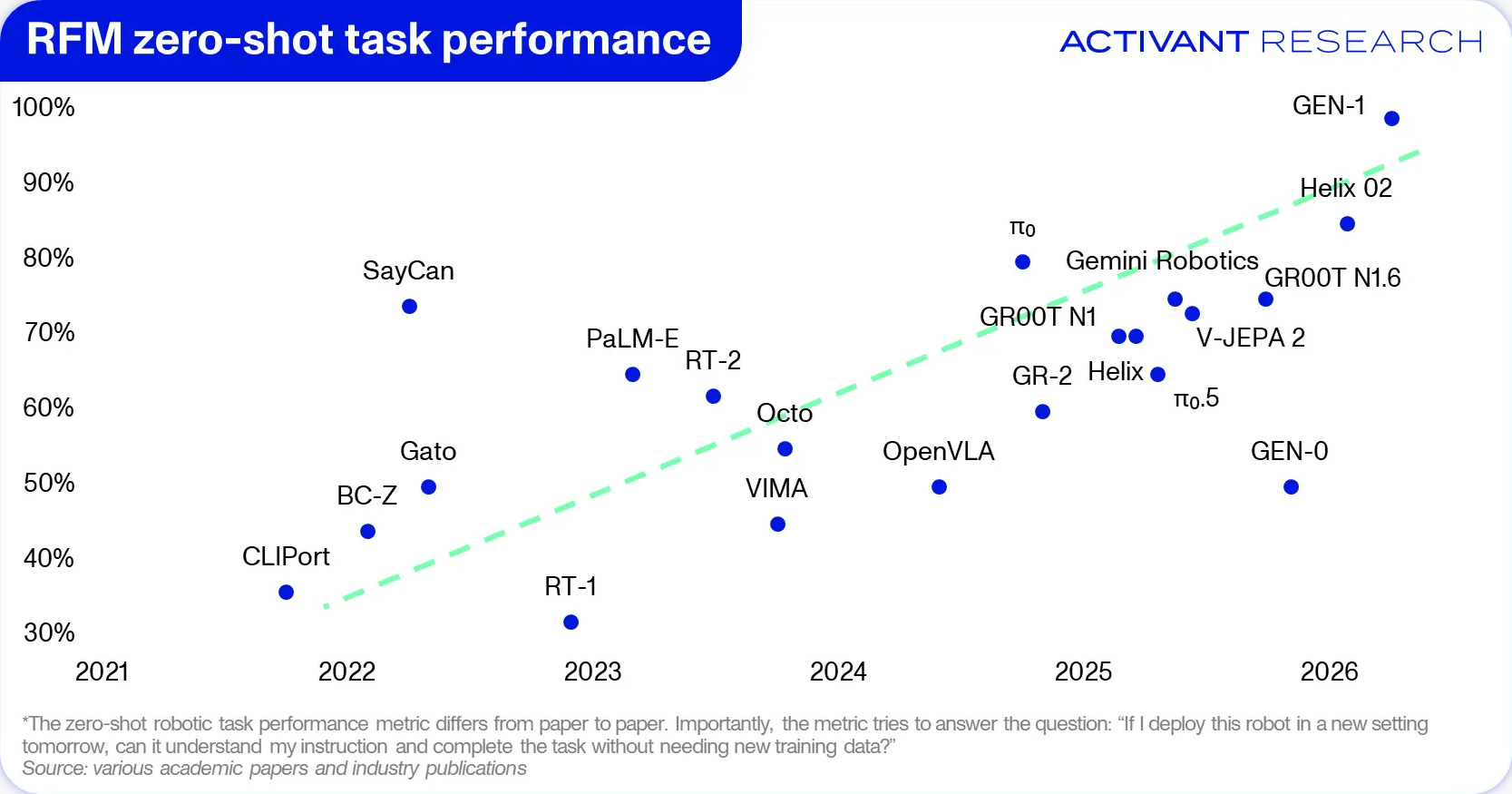

Progress then accelerated rapidly. In 2024, Physical Intelligence (π) released their 2B-parameter flagship model, π0, capable of folding laundry, assembling boxes and bagging groceries – all notoriously difficult problems.11 In February 2025, Figure released Helix, the first VLA capable of controlling the arms, hands, individual fingers, torso and head of a humanoid at high frequency, demonstrating that VLAs could scale from tabletop manipulation arms to full humanoid embodiments.12

Shortly afterwards, Nvidia released GR00T N1, an open-source 2B-parameter VLA for humanoids trained on a mix of real-world and synthetic data from its Omniverse and Cosmos platforms.13

VLA capabilities have progressively improved since 2022.

The trend is clear, but the question is whether the improvement is predictable.

Scaling Laws

In November 2025, Generalist AI (founded by researchers and engineers behind Google DeepMind’s PaLM-E and RT-2) released GEN-0, a robotic foundation model (RFM) trained on 270,000+ hours of real-world manipulation data – an order of magnitude more than any previous robotics training set.14 Their central finding was the observation of a “phase transition” in performance when their models surpassed 7B parameters, showing adherence to the same scaling laws that have underpinned the rise of LLMs.15 A first for RFMs: more data + more compute = better, more predictable performance.

Generalist AI unveiled their follow up model, GEN-1, in April 2026 and showed that it has crossed what they called a “mastery threshold”.16 Average success rates reached 99% across multiple dexterous tasks, up from the 64% achieved by GEN-0. GEN-1 could fold T-shirts 86 consecutive times without intervention, service robot vacuums over 200 consecutive times, and assemble boxes at ~3X the speed of the previous SOTA. Most significantly, GEN-1 could improvise when encountering unexpected situations outside of its training distribution, showing emergent behavior.

Scaling laws are what transformed LLMs from academic experiments into an investment thesis: they made progress predictable.17 There is increasingly more evidence to suggest that these laws do exist in robotics. In just over three years, we have moved from “a robot can sometimes pick up an object it hasn’t seen before” to “a robot can fold laundry and recover from unexpected failures for hours without intervention.”

After centuries of progress gated by human programming, AI has handed robotics the same gift it gave language: a predictable paradigm of improvement. Hardware can now begin to act with the sophistication of the humans it was built to assist, and the economic ramifications of that shift could be enormous.

The Robotics Market is Priced for Perfection

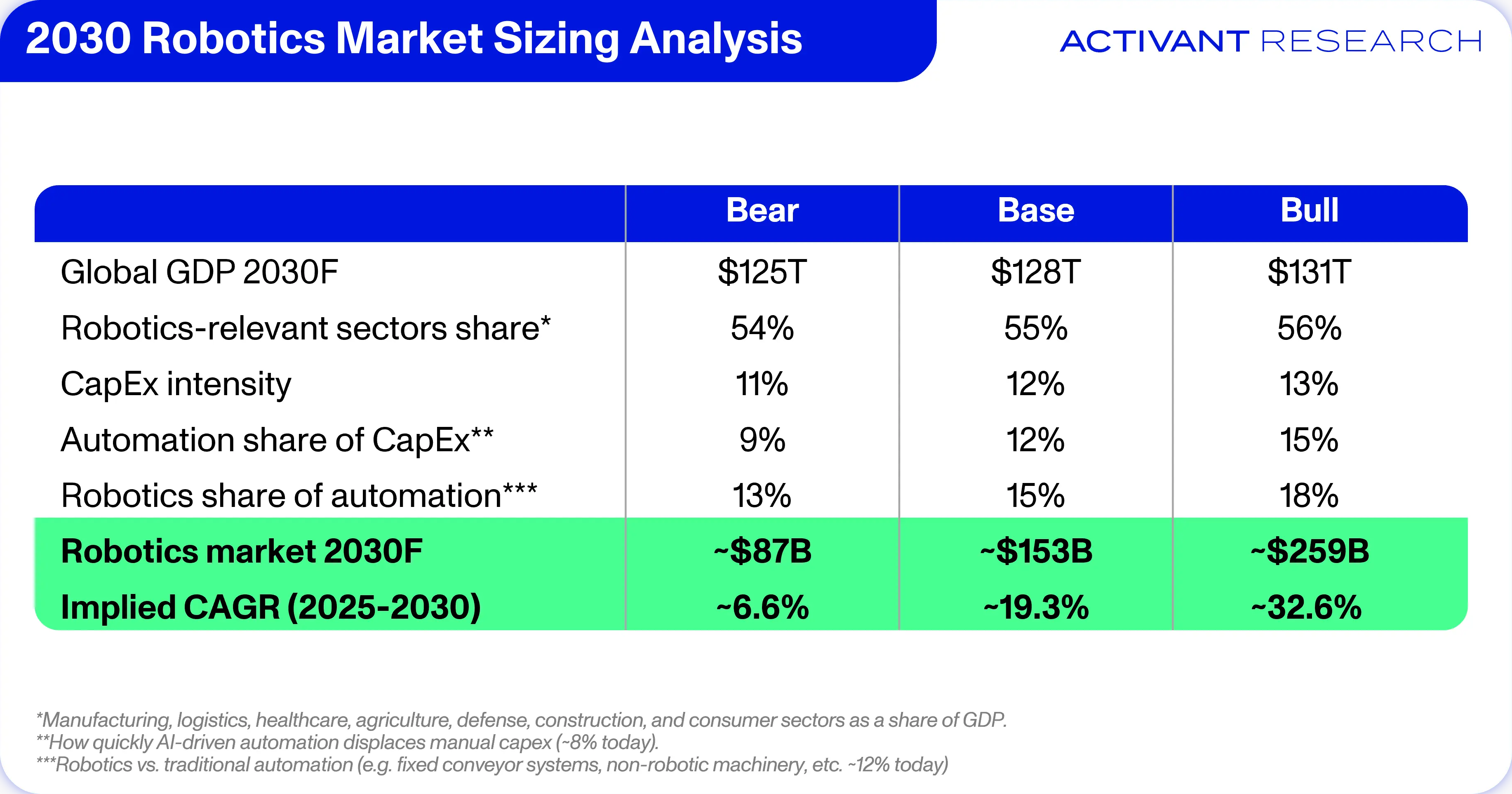

Take the manufacturing sector as an example: the installed base of robots is ~5 million units, while the number of manufacturing workers is 450 million.1819 With intelligence as the breakthrough for generalized robotics, the market could expand along a runway of ~100x the current scale. That’s deliberately exaggerated – robots won’t fully replace humans – but the point is the magnitude of the shift that could be ahead.

From a top-down, macroeconomic perspective, the size of the global robotics market is driven almost entirely by two variables: 1) how quickly automation captures a larger share of capex, and 2) how much of that flows to robotics. Both are functions of how quickly the bottlenecks constraining physical AI are overcome. Assuming 3% GDP growth, a 12% automation share of capex, and 15% robotics capture, we see the market growing to $153 billion by 2030.

The scaling laws set the direction, but the timing determines the price. If the bottlenecks constraining physical AI are overcome quickly, then automation’s share of capex accelerates and robotics captures a larger chunk of it: bull-case. If they prove too slow and capital-intensive to resolve: bear-case. The timeline through the bottlenecks is, quite literally, a market-sizing question.

The central problem for the robotics market today is that the bull case has likely already been priced in.

Where the Capital Is Landing

As the LLM cycle demonstrated, when scaling laws exist, capital follows. In 2025, $23.2 billion of investment flowed into robotics startups – around 4.5% of global venture funding for the year. Global robotics investment has already reached $21.6 billion as of early Q2 2026, representing ~10% of all VC investment for the year so far.20

Against this backdrop, consider how individual companies are being priced. Goldman Sachs projected the entire humanoid-specific market to be valued at $38 billion by 2035.21 Our base case sizes the full robotics market at ~$153 billion by 2030.22 Yet the combined valuation of the top five Western humanoid and RFM startups already exceeds $73 billion. Figure alone, at $39 billion, exceeds Goldman’s forecast and represents more than 25% of our 2030 base case. Those same startups have raised ~$4.6 billion in funding to deploy fewer than 400 units to date – almost $12 million in funding per unit deployed.23

What the Valuations Imply

At $39 billion and a 15x forward revenue multiple targeting a 2028-2029 IPO, Figure will need approximately $2.6 billion in ARR. With $1,000/month RaaS pricing, that requires ~215,000 units in continuous paid deployment. Figure’s high-volume manufacturing facility, BotQ, has ramped production from one robot per day to one per hour in under 120 days.24

At the stated hourly rate, annual production is ~8,760 units/year, against a stated four-year production target of 100,000.25 The manufacturing trajectory is real and accelerating, but ~215,000 units in continuous paid deployment is still a long way from current production throughput. Even at 100,000 deployments by 2029, the implied revenue multiple is 32.5x.

Tesla, with its deep balance sheet, manufacturing infrastructure, and sophisticated supply chain had a production target of ~5,000 Optimus humanoids in 2025.26 It shipped ~150 units. If one of the most vertically integrated manufacturers on the planet missed its production target by 97%, what execution assumptions are we embedding in startup pricing?

Physical Intelligence, at $11 billion pre-revenue, is priced as the Android of physical AI. The analogy is apt. Android was also pre-revenue when Google acquired it for $50 million in 2005.27 At the time, smartphones barely existed: the iPhone launched in 2007, and the first Android phone (T-Mobile G1) shipped the following year.2829 By 2010, Google had open-sourced Android with the goal of putting the internet in the palms of the masses, and it became the globally dominant mobile OS, attracting hardware manufacturers who could not compete with Apple’s vertical integration.

The goal of RFMs is the same: drive automation adoption by providing the universal brain that any robot manufacturer can install on their hardware for a fraction of the price of in-house development. The global operational stock of industrial robots currently stands at ~5 million units, growing at ~9% YoY.30 To justify current valuations, RFMs will need industrial robot penetration of 2.7%-6.2% with an estimated $500/month RaaS pricing-model.31 The gap between that ambition and current capability is narrowing but still remains wide.

These valuations are not irrational. They are bets on a specific timeline through the structural bottlenecks. The question is whether that timeline is realistic.

The Bottlenecks

The investment thesis for general purpose robotics rests heavily on an analogy to LLMs. If RFMs are following the same trajectory, then investing in the leading RFM companies today (Physical Intelligence, Skild AI, Generalist AI, Rhoda AI, etc.) is the equivalent of investing in OpenAI or Anthropic in 2020/2021.

We believe the same scaling laws that underpinned the LLM revolution exist in robotics. But acknowledging the scaling laws only tells us the direction of progress, not the speed. In physical AI, four distinct bottlenecks constrain how fast we can ride the scaling curve, each making the journey longer and more capital-intensive than the LLM analogy implies.

1. Data Acquisition

LLMs are trained on the internet, which is vast and freely available. RFMs require physical interaction data, which is notoriously scarce, expensive, embodiment-specific, and often proprietary. Generalist’s 500,000 hour robotic-manipulation dataset, reportedly the world’s largest, is still orders of magnitude smaller than GPT-3’s task space. Generalist’s data acquisition strategy of using low-cost wearable devices on a network of humans, rather than expensive teleoperation collection, is promising (growing at 10,000 hours/week), but the rate at which physical interaction data can be collected remains a fundamental constraint on scaling velocity.

2. Output Deployment

LLM outputs are digital and thus instantly deployable anywhere with an internet connection. RFM outputs must control physical hardware subject to latency requirements, real-world unpredictability, and safety constraints. Every increment of capability must clear a higher deployment bar before it generates commercial value.

3. Hardware Heterogeneity

LLMs benefit from a largely homogenous substrate: Nvidia GPUs processing text. RFMs must generalize across wildly diverse embodiments – from 6 degrees of freedom (DoF) arms to 30+ DoF humanoids to quadrupeds – each with different actuators, sensors and dynamics. The scaling laws may hold within a given embodiment, but generalizing across embodiments introduces friction that slows the path from lab to deployment.

4. The Sim-To-Real Gap

There is no LLM-equivalent to this problem. A LLM trained on text generates text. A robot trained in a simulated environment must transfer its learned behaviors to a physical world that doesn’t perfectly match the simulator. This imperfection, referred to as the sim-to-real gap, has been identified as “one of the most critical and long-standing challenges in robotics”.32 World models are emerging as a promising path forward: rather than relying on human-engineered simulators, companies like General Intuition learn physical dynamics directly from action-labeled video, producing simulations that transfer more naturally to robotic form-factors. Figure recently demonstrated zero-shot sim-to-real transfer for perception-conditioned stair walking, with no real-world fine-tuning or operator intervention.33 While the gap is narrowing, it has not yet been closed.

The scaling laws appear to be real. The question is whether the bottlenecks constraining physical AI can be overcome on the timelines and at the capital costs that current valuations imply.

We’ve Seen This Before

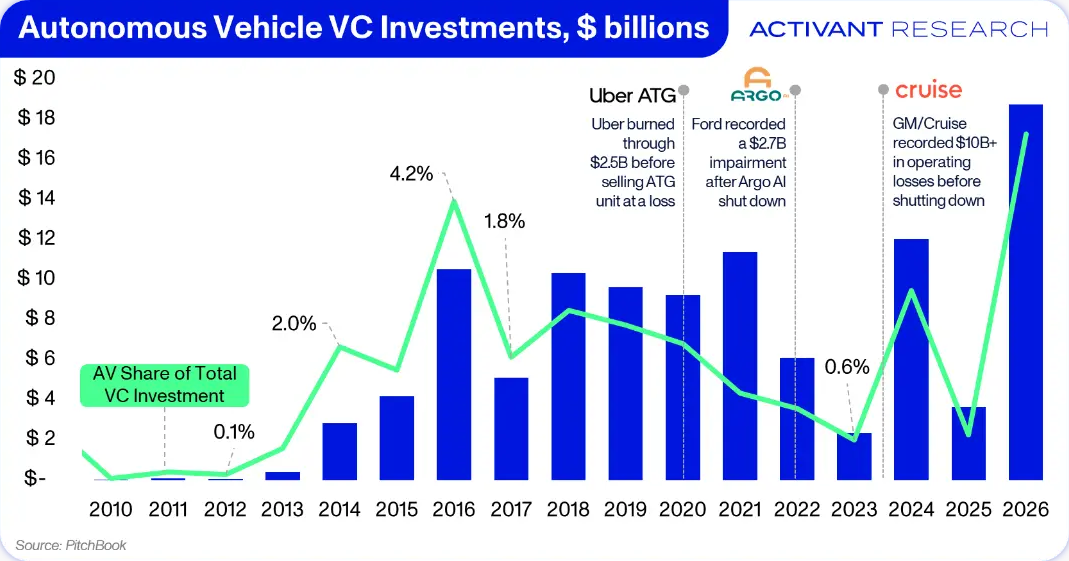

This is not the first time venture capital has made concentrated bets on AI-powered physical systems. Between 2016 and 2021, autonomous vehicle (AV) startups attracted tens of billions in investment on an identical conviction: the technology works in controlled settings, AI is accelerating, and commercialization is imminent.

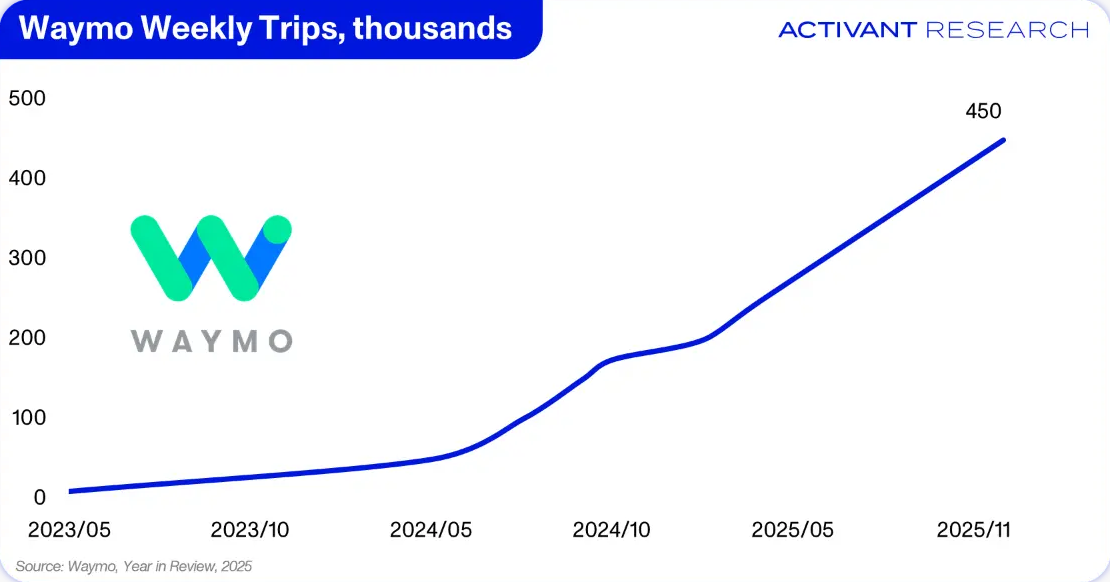

GM/Cruise accumulated more than $10 billion in operating losses; Ford recorded a $2.7 billion impairment when Argo AI shut down; and Uber ATG burned through $2.5 billion before selling to Aurora.34 Waymo’s expansion proves that the tech did, in fact, work, but it took over a decade, and claimed a significant number of well-funded casualties.35

The lesson of the AV cycle is not that the technology was wrong. It is that the timeline from “cool demo” to commercial deployment was severely underestimated, partly because the data and scaling challenges of operating in the physical world proved harder than the simulations suggested.

Who Wins While the Bottlenecks Hold?

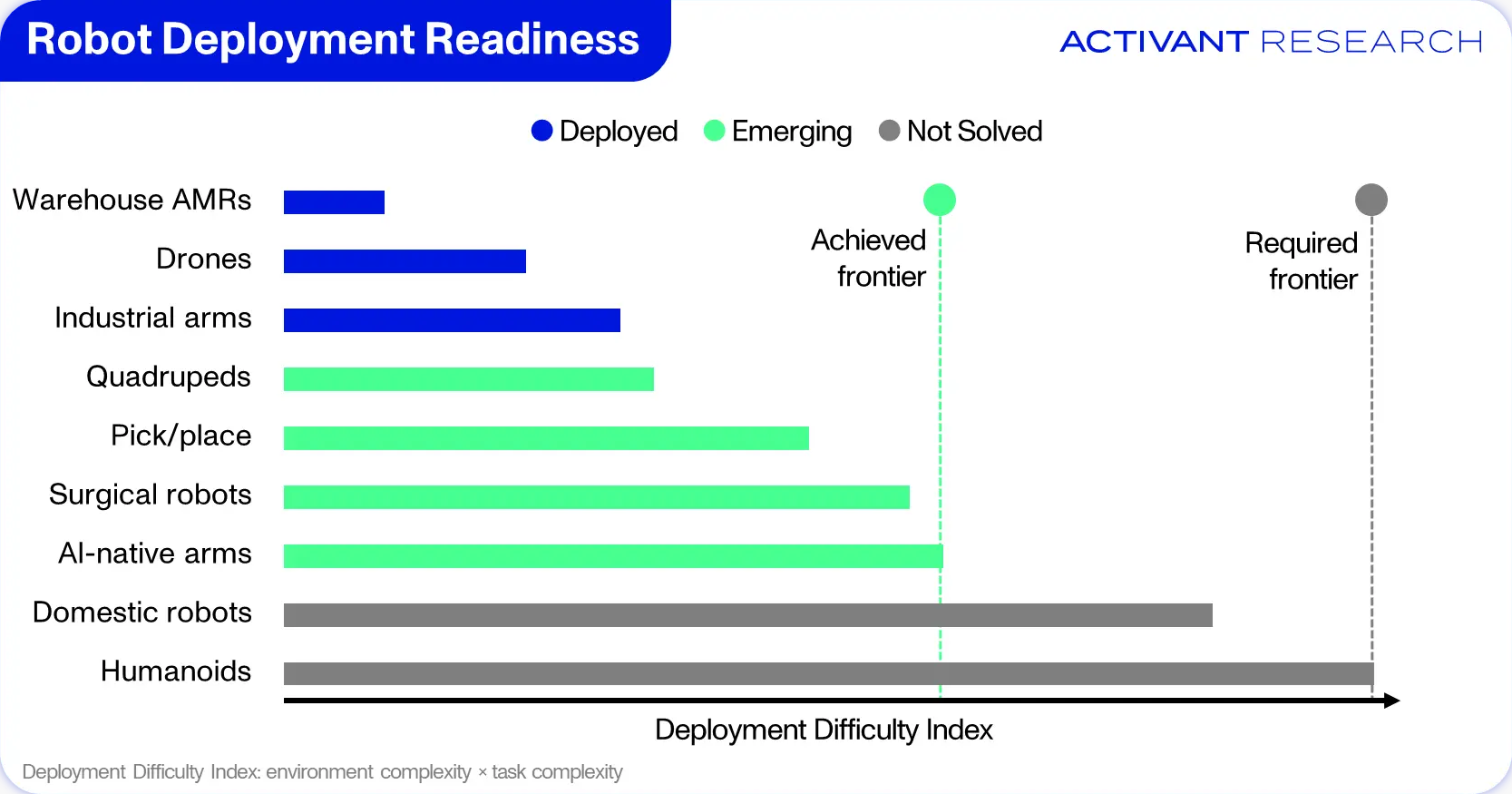

The companies generating real revenue in robotics today have one thing in common: they build specialized machines optimized for specific, high-volume tasks. For a large proportion of robotics applications – where tasks have some degree of repetition, environments are at least semi-structured, and required throughput is high – commercial deployment is achievable today.

Under these conditions, specialized robots don’t simply do the same job cheaper than a humanoid would. Instead, they redefine the job entirely. Consider agricultural robotics company Carbon Robotics’ autonomous weeding system, LaserWeeder G2. The system attaches onto a tractor and eliminates 100,000 weeds/hour with millimeter precision at an 80% cost reduction, all while using no pesticides or mechanical cultivation.36 A humanoid would approach this task the same way humans have approached it for centuries: bending over, identifying each weed, and pulling them out one-by-one. The specialized machine eliminated that motion altogether by swapping hands for lasers, walking for rolling, and human judgment for computer vision. The result is a fundamentally different category of productivity, not just a better farm worker.

Every time industry has automated a physical task at scale, it has chosen task-specific optimization over human-like form. We didn’t build mechanical horses for transportation; we built cars. We didn’t build humanoids to wash dirty dishes in restaurants, we built dishwashers.37

The main thesis behind humanoids is “human shapes for human places”. This is not a rebuttal of that thesis – it makes complete sense in theory. It is context for understanding why the companies generating real revenue today are simultaneously building the data assets that will matter most if and when the bottlenecks clear.

So, what does an attractive robotics business look like while the bottlenecks hold? We believe there are two key differentiators:

Proprietary data generation at scale: A company’s business model should generate physical interaction data that compounds with every deployment. Intuitive Surgical’s 10M+ completed procedures; Anduril and Shield AI’s classified operational intelligence; Amazon Robotics’ fleet-level learning across more than a million deployed warehouse robots; and Simbe’s five million hours of fully autonomous operation are data assets that no competitor can replicate from a standing start.383940 These business models go beyond revenue streams; they are building the training corpora for tomorrow’s foundation models as a byproduct of today’s operations. Critically, the data flywheel only spins if the revenue model is recurring. One-time hardware sales don’t generate ongoing data. The strongest positions combine hardware deployment with software licensing or RaaS models that ensure every unit in the field keeps generating data and revenue simultaneously.

Low hardware commoditization risk: Competitive advantages must be rooted in data, software, or regulatory barriers, not in hardware assembly. If a company’s moat rests primarily on building the physical machine, a Chinese manufacturer can and will replicate it at a fraction of the cost. iRobot’s Chapter 11 filing is the strongest example: deployment at scale + no technical moat = maximum exposure to Chinese price competition.41 Defense robotics sits at the other end of the spectrum: security clearances and classified programs create absolute barriers that no competitor can circumvent.

The pattern is clear: the companies that survive and grow are those whose value lives in what the robot knows, not what it’s made of. Companies that meet both criteria hold the strongest position in robotics regardless of which timeline plays out. If RFMs scale quickly, they have the existing distribution and proprietary data for deployment fine-tuning. If the bottlenecks hold, they have real revenue.

Where We Stand

We believe the winners of the robotics market will be companies using new intelligence to transform traditional automation while simultaneously generating proprietary data at scale and building recurring revenue. There is a broad landscape of businesses that are not waiting for the bottlenecks to clear – they are clearing them, one deployment at a time.

Humanoid deployment at scale is coming, but the bottlenecks are still binding. The companies best positioned for the future are the ones already building the data assets that will power it.

Footnotes

-

Goldman Sachs, The global market for humanoid robots could reach $38 billion by 2035, 2024. ↩

-

S&P Capital IQ. ↩

-

Al-Jazari, The Book of Knowledge of Ingenious Mechanical Devices, 1206. ↩

-

Leonardo da Vinci, Leonardo da Vinci Inventions, 1490. ↩

-

Joseph Marie Jacquard, Jacquard Loom, 1804. ↩

-

Joseph Engelberger and George Devol, Unimate – The First Industrial Robot, 1961. ↩

-

Universal Robots, Teradyne Announce Agreement to Acquire Universal Robots, 2015. ↩

-

Food and Drug Administration, 510(k) Summary – Intuitive Surgical, Inc., 2000. ↩

-

Google DeepMind, RT-2: Vision-Language-Action Models Transfer Web Knowledge to Robotic Control, 2023. ↩

-

Google DeepMind, RT-1: Robotics Transformer For Real-World Control At Scale, 2022. ↩

-

Physical Intelligence, π0: A Vision-Language-Action Flow Model for General Robot Control, 2024. ↩

-

Figure, Helix: A Vision-Language-Action Model for Generalist Humanoid Control, 2025. ↩

-

Nvidia, GR00T N1: An Open Foundation Model for Generalist Humanoid Robots, 2025. ↩

-

Generalist AI, GEN-0: Embodied Foundation Models That Scale with Physical Interaction, 2025. ↩

-

OpenAI, Scaling Laws for Neural Language Models, 2021. ↩

-

Generalist AI, GEN-1: Scaling Embodied Foundation Models to Mastery, 2026. ↩

-

Activant Research, AI Infrastructure: Compute (1/4), 2026. ↩

-

IFR, World Robotics 2025 Report, 2025. ↩

-

UNIDO, Manufacturing jobs as a share of total employment, 2025. ↩

-

Ibid. ↩

-

Goldman Sachs, The global market for humanoid robots could reach $38 billion by 2035, 2024. ↩

-

Activant Research, Global Robotics Market Size Analysis, 2026. ↩

-

PitchBook. ↩

-

Figure, Ramping Figure 03 Production, 2026. ↩

-

Figure, BotQ: A High-Volume Manufacturing Facility for Humanoid Robots, 2025. ↩

-

Tesla, 2024 Q4 Earnings Call, 2025. ↩

-

Android Wiki, Android History, 2026. ↩

-

Apple, Apple Reinvents the Phone with iPhone, 2007. ↩

-

T-Mobile, T-Mobile Unveils the T-Mobile G1, the First Phone Powered by Android, 2008. ↩

-

IFR, World Robotics 2025 Report, 2025. ↩

-

Activant Research, Robotic Foundation Model Market Penetration Analysis, 2026. ↩

-

Annual Review of Control, Robotics, and Autonomous Systems, 2026. ↩

-

Figure, Ramping Figure 03 Production, 2026. ↩

-

Uber, Press Release, 2020. ↩

-

Waymo, Year in Review, 2025. ↩

-

Carbon Robotics, LaserWeeder G2, 2026. ↩

-

Siddharth Ramakrishnan (Scale Ventures), The Case Against Humanoids, 2026. ↩

-

Ibid. ↩

-

Activant Expert Network. ↩

-

Amazon, Amazon has more than 1 million robots that sort, lift, and carry packages, 2025. ↩

-

iRobot Corporation, Order and Final Decree, Case No. 25-12197 (BLS), 2025. ↩

Disclaimer: The information contained herein is provided for informational purposes only and should not be construed as investment advice. The opinions, views, forecasts, performance, estimates, etc. expressed herein are subject to change without notice. Certain statements contained herein reflect the subjective views and opinions of Activant. Past performance is not indicative of future results. No representation is made that any investment will or is likely to achieve its objectives. All investments involve risk and may result in loss. This newsletter does not constitute an offer to sell or a solicitation of an offer to buy any security. Activant does not provide tax or legal advice and you are encouraged to seek the advice of a tax or legal professional regarding your individual circumstances.

This content may not under any circumstances be relied upon when making a decision to invest in any fund or investment, including those managed by Activant. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Activant. While taken from sources believed to be reliable, Activant has not independently verified such information and makes no representations about the current or enduring accuracy of the information or its appropriateness for a given situation.

Activant does not solicit or make its services available to the public. The content provided herein may include information regarding past and/or present portfolio companies or investments managed by Activant, its affiliates and/or personnel. References to specific companies are for illustrative purposes only and do not necessarily reflect Activant investments. It should not be assumed that investments made in the future will have similar characteristics. Please see "full list of investments" at activantcapital.com/companies/ for a full list of investments. Any portfolio companies discussed herein should not be assumed to have been profitable. Certain information herein constitutes "forward-looking statements." All forward-looking statements represent only the intent and belief of Activant as of the date such statements were made. None of Activant or any of its affiliates (i) assumes any responsibility for the accuracy and completeness of any forward-looking statements or (ii) undertakes any obligation to disseminate any updates or revisions to any forward-looking statement contained herein to reflect any change in their expectation with regard thereto or any change in events, conditions or circumstances on which any such statement is based. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking statements.