B2B Commerce — April 30, 2024

It's Time Local Went Global

Real-time Payments

B2B transactions made up 97% of the ~$156 trillion in cross-border payment flows in 20231 and, according to UBS estimates, took 2-5 days to settle at an average cost of 6.2%.2 This is incongruous in a world where real-time payments (RTP) are transforming the payment landscape, particularly in domestic markets in developing economies (like Brazil and India), with settlement times decreasing to seconds and costs reduced by 50-90%.

A Market Ripe for Disruption

The global payments market recorded revenues of $2.2 trillion in 2022, an all-time high and up 11% for the year.3 With the notable exception of China, where payment revenues declined 3% in 2022, all other regions globally (North America, Latin America, Europe, Middle East, and Asia ex China) grew at double-digit rates.4 About half of this revenue growth came from rising interest rates, but fees still make up more than half of all payment revenues.5 When one considers that domestic payments cost anywhere between 30bp and 300bp depending on the payment rails used (ACH or card), and international payments costs (excluding foreign exchange fees) range from 65bp to 450bp,6 there is a significant profit pool to be disrupted.

Online payment platforms Square and Stripe used technology to bring innovation, convenience, and efficiency to sleepy local payments markets. They, and other payment facilitators (payfacs), have opened markets to many more merchants, lowered costs for everyone, and introduced a wide array of products and services that allows them to monetize payment flows. These offers range from hardware (like Toast’s point-of-sale (POS) hardware) to related software (such as Stripe’s billing or fraud and risk management solutions or Square’s inventory management or marketing products). We have also seen the rise of payfac-as-a-service (PFaaS) solutions to allow non-fintech companies to offer payment acceptance to their customers. Shopify, for example, is powered by Stripe.7

Payfacs disrupted payments markets by overlaying technology and services onto existing payment networks (or rails). Real-time payments, however, are disrupting markets around the world using an entirely new set of rails.

Real-Time Payments

Real-time payments (RTP) are account-to-account (A2A) financial transactions that are initiated, cleared, and settled immediately–typically within seconds. These payments run on RTP networks, which both central banks and commercial banks have designed to connect financial institutions and enable them to offer faster and cheaper payment solutions to consumers and merchants outside of traditional payment infrastructure or rails (cash & check, ACH, wire, card).

The first RTP network was launched in Japan in 1973,8 but it is only over the past five years that growth has exploded. Today, there are over 80 RTP networks operating around the world that accounted for 195 billion transactions in 2022 (18% of all global electronic payments transactions).9 ACI estimates that this market will grow at a compound annual growth rate (CAGR) of 21% to reach 512 billion transactions by 2027, representing 28% of all payments transactions. Most of this growth will come from EMEA (21% CAGR) and Latin America (29% CAGR).

Emerging economies such as India and Brazil account for the majority of RTP transactions. These two countries alone represented ~61% of global RTP transactions in 2022.10 India launched their RTP network, Immediate Payment Service (IMPS), in 2010 but it was only in 2016 that growth really exploded with the rollout of their Unified Payments Interface (UPI). The system enabled real-time payments across numerous channels (P2P, C2B, B2B, and C2G) through mobile numbers, QR codes, and virtual IDs.11 In 2022, UPI facilitated ~90 billion transactions representing ~45% of all transactions in India.12 Brazil’s PIX instant payments network is driving a similar change in that country, as is the NIP system in Nigeria where cash transactions fell from 95% in 2019 to 80% in 2022.13

Developed markets have been slower to adopt RTP networks, with Europe and the U.S. processing only 13 billion (7% of all transactions) and 4 billion (2% of all transactions) transactions respectively in 2022.14 The U.S. has three established RTP networks: The Clearing Houses’ (TCH) RTP network, Early Warning Services’ Zelle mobile peer-to-peer instant payment application, which both launched in 2017, and most recently the Federal Reserve Bank’s FedNow, which launched in 2023. TCH’s RTP network has seen a significant increase in growth after a slow start, with 2Q23 volumes representing a 5.8x year-on-year (YOY) increase. Zelle, on the other hand, has seen substantial growth since launch and is the clear leader in terms of P2P real-time payments. Zelle is owned by a consortium of large U.S. banks that guarantee distribution by providing easy access for their large customer bases.

RTP currently represents 12% of all credit transfers in the Single Euro Payments Area (SEPA) and McKinsey estimates this share could double by 2027, or even increase four-fold to ~45% of payments transactions if regulators pass anticipated legislation to encourage adoption of RTP.15

RTP will undoubtedly grow to become the preferred payments option in countries around the world. The benefits of RTP networks and transactions are real and compelling. They offer:

- lower costs as interchange fees are reduced or bypassed entirely;

- increased security by enabling bi-directional communication in a secure system, introducing two-factor (or multi-factor) authentication, and device binding and confirmation;

- reduced fraud risk by conforming to ISO20022 (which enables financial institutions to send data-rich sets with each transaction);

- greater visibility into financial positions, reducing the risk of overdraft fees or other penalties,

- better cash flow management by expediting refund and disbursement processes;

- opportunities for value-added services that customers appreciate, like QR payments, split payments, or request-to-pay options.

As one considers the many benefits of RTP, it is important to recognize that all real-time payments are irrevocable and can’t be reversed or “de-authorized” by the payor, which places a premium on fraud and risk management.

Against this backdrop of widespread adoption and very encouraging growth, it is interesting to observe that this has largely been driven domestically, while most payment volumes are cross-border and B2B.

Cross-Border Payments Offer a Unique Opportunity

Cross-border payment flows continue to grow at double-digit rates, generating $240 billion in revenues for payments providers in 2022, with B2B payments making up 69% of total revenues (on 97% of the payment flow).16 Consumer payments are more profitable and are projected to grow more rapidly over the next 5 years.17 The U.S./Latin America corridor, the largest in the world for C2C remittances, is expected to continue growing robustly given family remittances and U.S. humanitarian aid.18

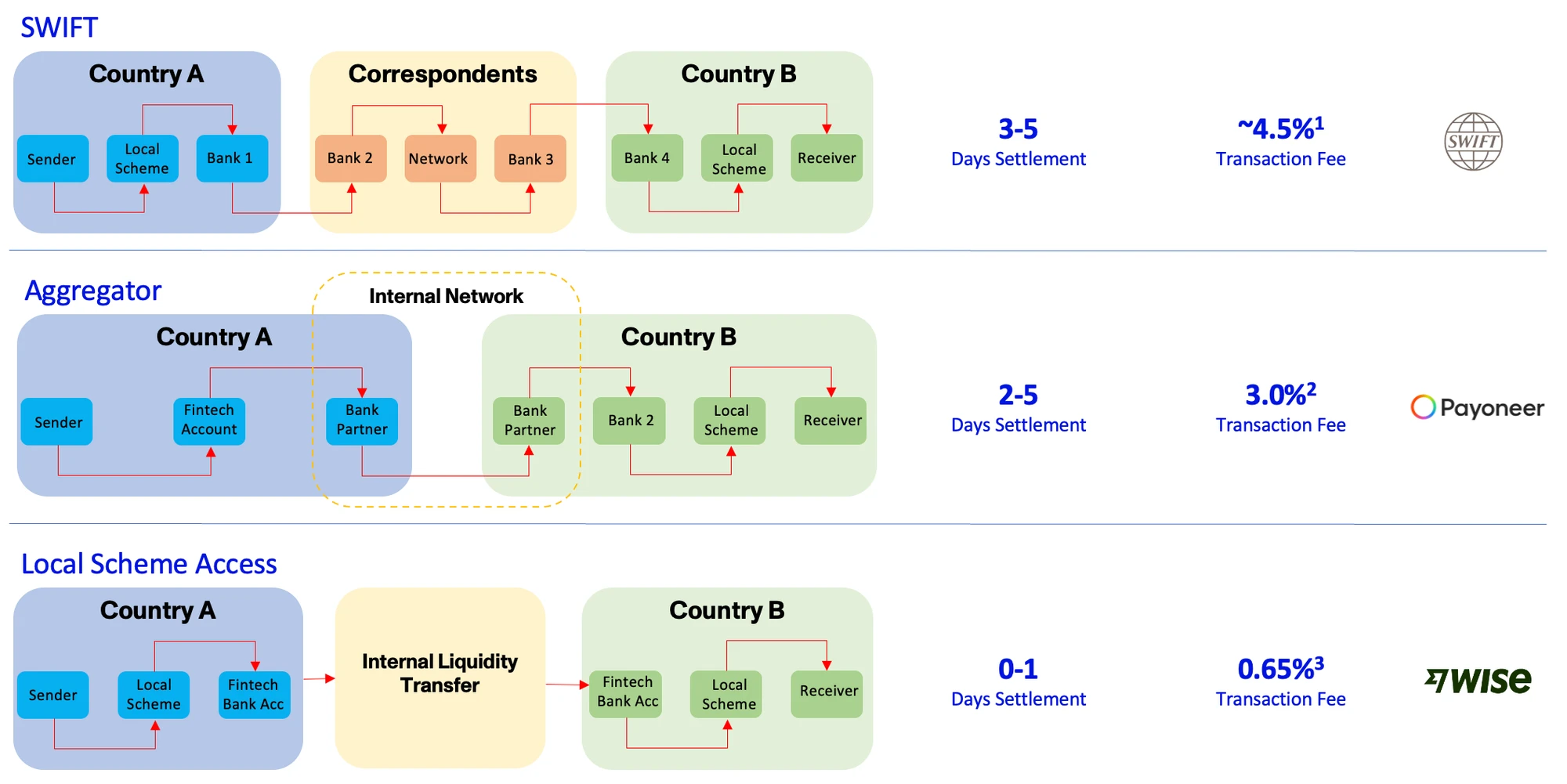

Despite the volume of capital flows and benefits that RTP could bring, cross-border payments continue to operate on traditional rails or networks designed to handle wires, credit and debit cards, and international ACH transactions. These traditional networks are:

- slow, with wire and card transactions taking 2-5 business days to settle;

- expensive, with costs ranging from 0.65% to 9.85%19 of the transfer or payment;

- less secure than new networks operating to the ISO20022 standard as the messaging format of legacy rails provides little information regarding transactions;

- opaque as the long settlement times limit visibility into true liquidity positions.

The diagram below illustrates some of these disadvantages by providing an overview of the current cross-border payment process flows, the associated costs, and average settlement times.

RTP networks have the potential to address all the issues identified, just as they do in local markets, by linking domestic networks across borders. Singapore connected its PayNow service with Thailand’s Promptpay system to launch the first true cross-border RTP network, and later linkedPayNow with India’s UPI service. The Bank of International Settlements Innovation Hub (BISIH) launched its Nexus project in 2022 and built a working prototype to connect the test systems of three established RTP networks – the Eurosystem’s TARGET Instant Payment Settlement (TIPS) system, Malaysia’s Real-Time Retail Payments Platform (RPP), and Singapore’s Fast And Secure Transfers (FAST) system– across borders. Similarly, the Immediate Cross-Border Payments (IXB) pilot was launched as a collaboration between U.S.-based TCH and Europe’s EBA.20 The pilot linked TCH’s RTP network in the U.S. with ECB Clearing’s RT1 network to process $:€ transactions and was designed to add additional currency corridors after the planned commercial rollout in 2023.

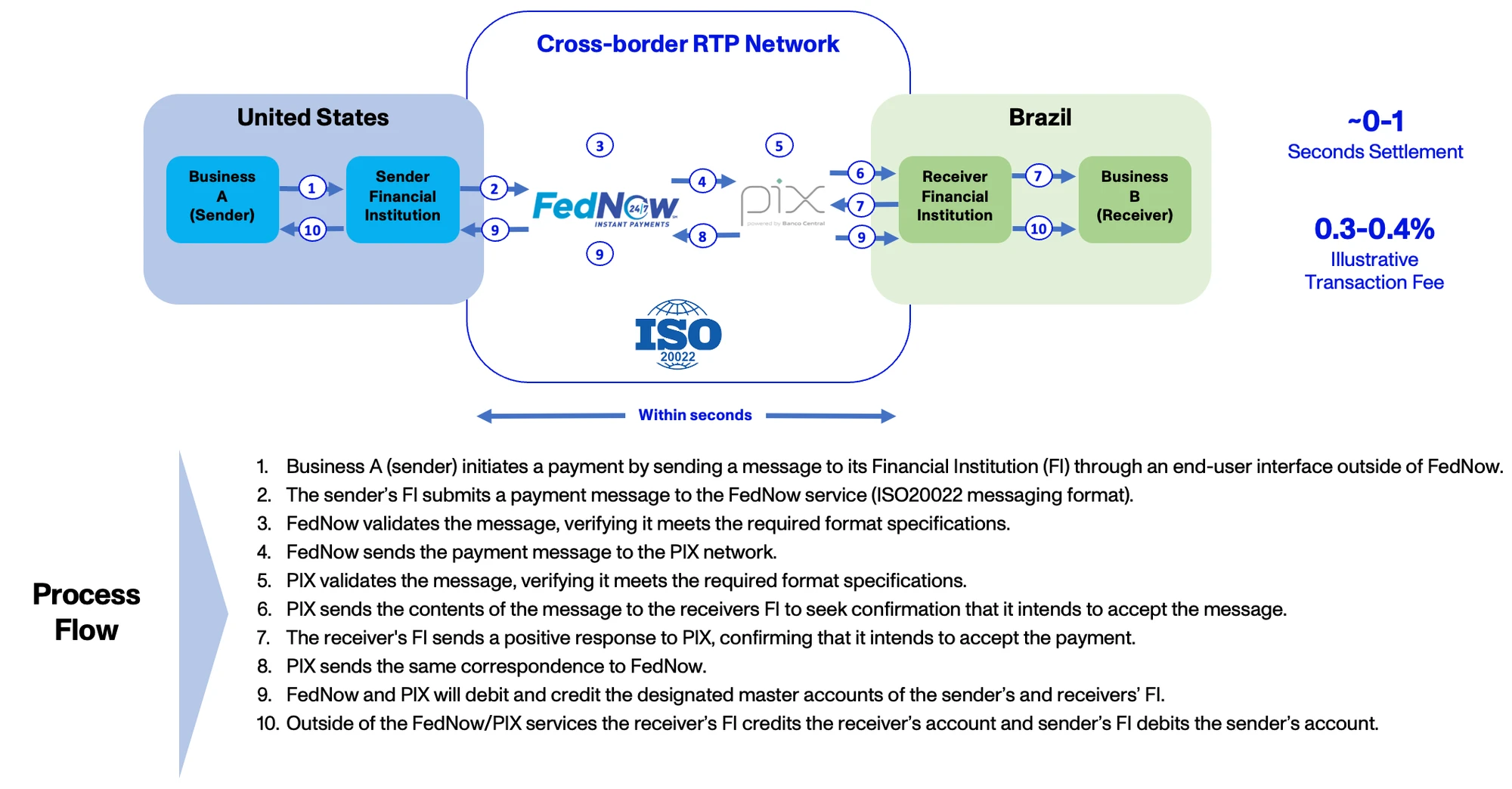

To date, however, no major trading corridors have implemented a commercial solution. Imagine if FedNow, the U.S. Federal Reserve’s real-time payment rail network launched in July 2023, were to link to Brazil’s PIX network to facilitate RTP flows between those countries.

The FedNow rails are not a finished product and currently aren’t interoperable with other networks, but with this functionality FIs could deliver fast, cheap, data-rich, and transparent cross-border transactions. The large-scale adoption of cross-border B2B RTPs will, however, be limited in the short-term by the need to align:

- regulatory frameworks as each country has unique frameworks, data laws, security requirements, and consumer protection laws that need to be adhered to;

- interoperability standards between networks in different countries. The global move to the ISO20022 messaging standard should help alleviate this;

- settlement systems, as real-time payments require systems that can handle multiple currencies concurrently. These systems vary from country to country;

- fraud/Anti-Money Laundering (AML)/Know-Your-Customer (KYC) requirements to handle real-time transactions that are irreversible. Fraudulent transactions made up ~79% of the 1.52% of all B2B transactions charged back in 2021;21

- financial institution liquidity systems to handle immediate settlements 24/7/365.

RTP Market Landscape

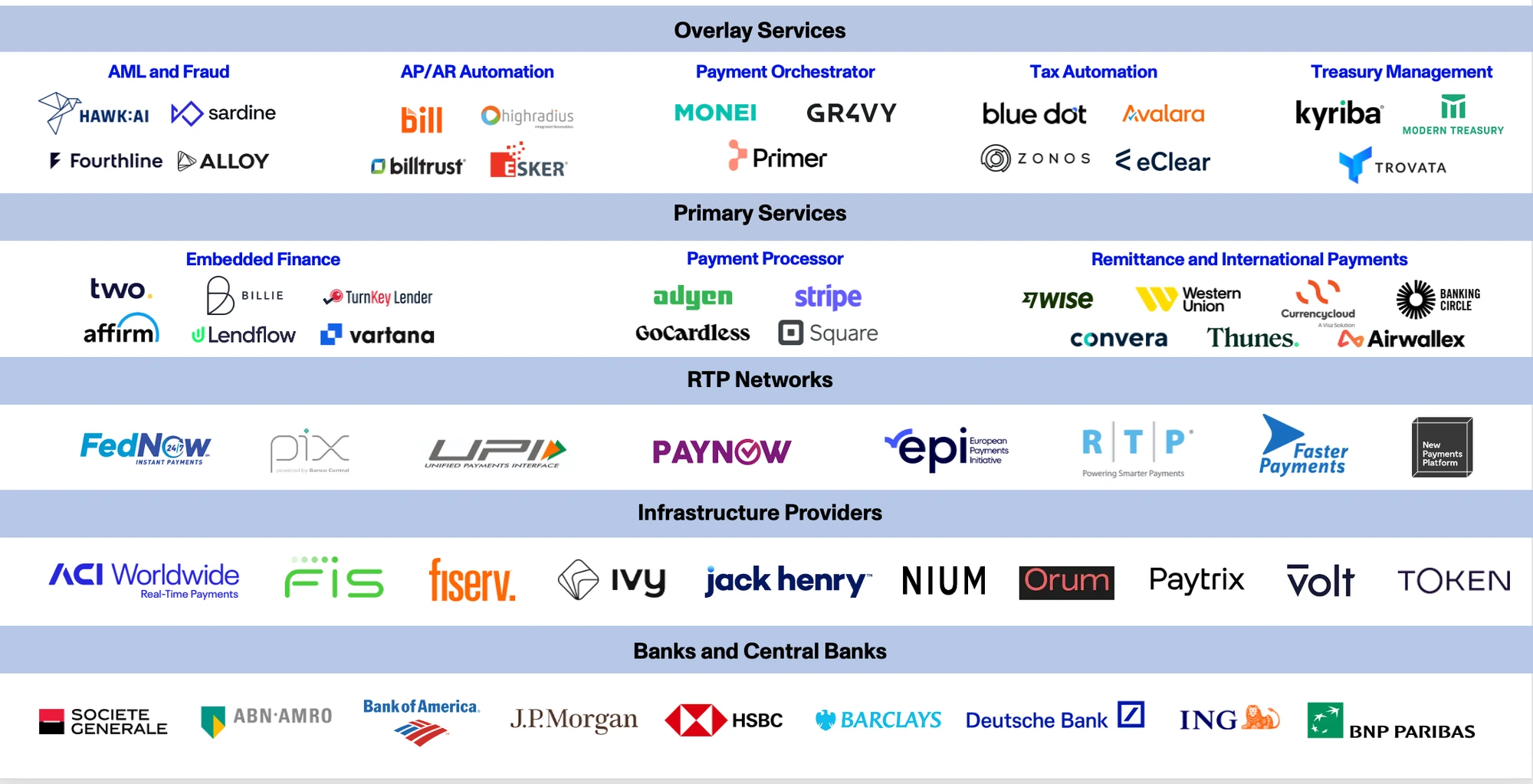

We found it helpful to think about the RTP market as consisting of five distinct layers:

- Banks and Central Banks

- Infrastructure Providers

- RTP Networks

- Primary Services

- Overlay Services

The primary and overlay service players utilize the infrastructure of the connected RTP networks to provide value-added services such as payment processing, remittance, treasury management, and KYC/AML/fraud detection. We see the increased adoption of cross-border RTPs as a net positive for many of the primary and overlay service providers. However, the one specific service area that we believe would be under threat from the growth of cross-border RTP is the remittance and international payment processing businesses. If central banks can successfully connect through cross-border networks and process transactions cheaply, the business case for low-cost remittance and international payments would fall away.

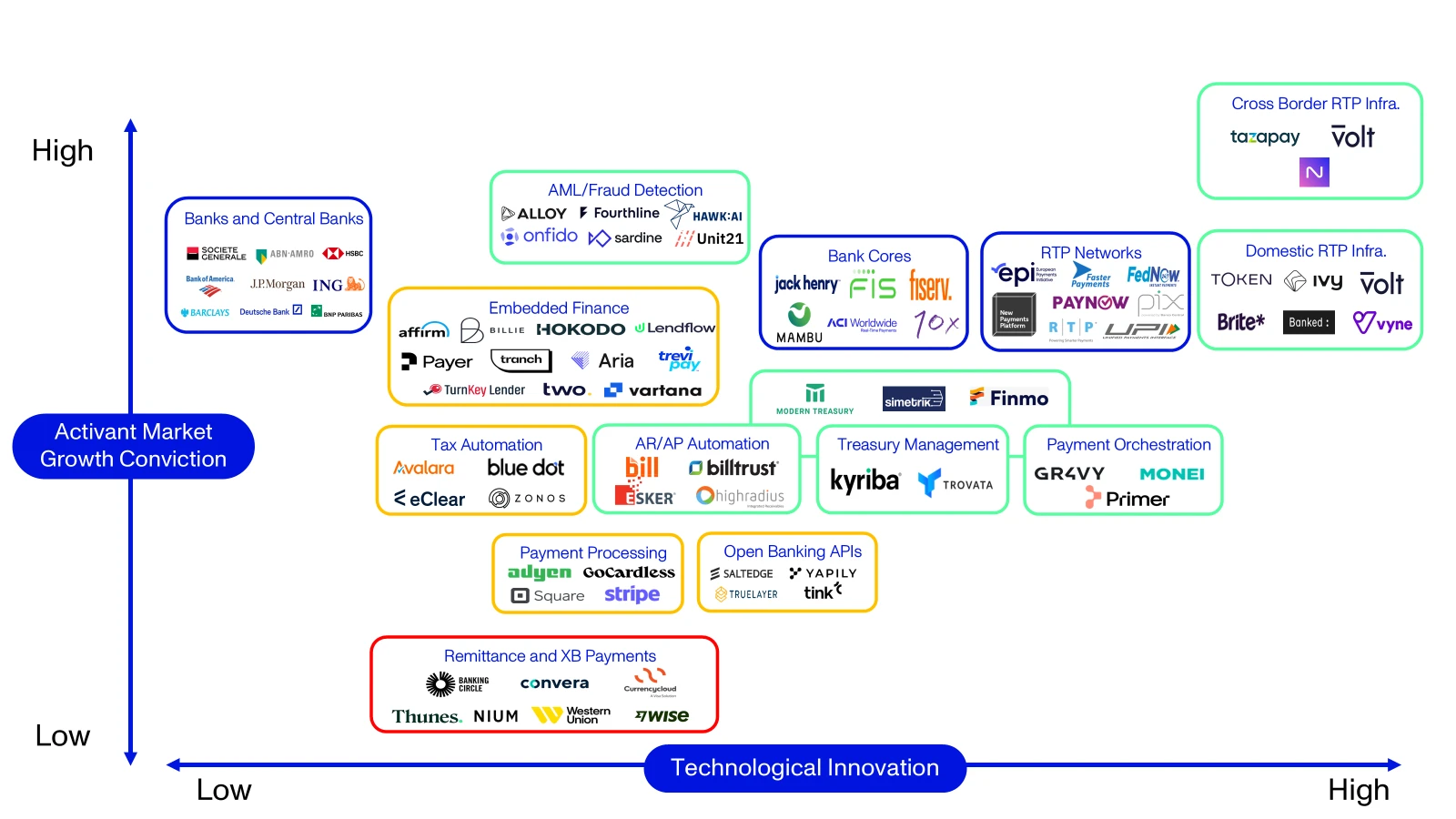

Our Activant Thesis Map, shown on the next page, summarizes our market growth conviction and the degree of technological innovation for each of the distinct clusters of companies. We are most excited about the growth prospects of RTP infrastructure providers and the overlay service providers that build on or enable RTP transactions. These sectors are shown in green on the thesis map. We believe that RTP networks will grow and take market share away from many of the current payment rail systems, but these are often national solutions developed by central banks (like FedNow in the U.S.) or networks of banks (like the Zelle network in the U.S. or the European Payments Initiative in Europe) so we excluded them from consideration. Similarly, we believe that the FIs holding the primary account relationships will benefit at the expense of remittance and cross-border payments players if they offer RTP options that are competitively priced.

Opportunities Going Forward

We identify promising opportunities among infrastructure players and the providers of overlay services:

- Domestic and Cross-Border RTP Infrastructure players are responsible for creating the back-end technology that connects the banks to RTP networks, and RTP networks across borders in some instances. While there is a use case for domestic RTP transaction facilitators like Brite, Vyne, Banked and others, the real margins come from cross-border transactions. As spreads are reduced on domestic transactions, going global presents the opportunity to target profit pools that generate billions in net revenue for incumbent operators.Volt, Navro, Tazapay and other new entrants targeting this market stand to benefit from increased transaction flow across RTP rails.

“We’re fast moving into an era where real time is the only time. For too long settlement times have been dictated and constrained by legacy infrastructure. Real-time account-to-account payments are changing this. When, not if, the issues of standardization and interoperability are solved for, we can start talking about a true real-time revolution for payments.”

- Traditional Core Banking Systems and infrastructure players like ACI Worldwide, FIS, Fiserv and Jack Henry all provide access to RTP networks, but they aren’t focused on the future of RTP and RTP connectivity in the same way as the RTP infrastructure players.

- AML/Fraud Detection is critical and likely to become even more so as fraudsters target the opportunities for instant settlement and the ability to rapidly move money from account to account. B2B transactions, and particularly those that are cross-border, are larger than C2C and C2B payments and typically require increased transaction verification and supplier identification. According to the 2019 Federal Reserve Payments Study,22 the average B2B ACH and wire transactions were $9,000 and $4.5 million, respectively. This compares to average C2B ACH and wire transaction sizes of $719 and $119,000, respectively. The average cross-border wire transfer was $3.8 million. As a result, there is a clear need for sufficient AML and fraud detection capabilities working alongside the fast and efficient RTP network. Activant is an investor in Sardine, and we think that Onfido, Unit21, Alloy and others offer interesting and effective solutions.

- Overlay Services built to provide solutions addressing a myriad cash and payments related needs – from AR/AP automation to Treasury Management and Payments Orchestration – offer opportunities to improve the efficiency of payment flows through connections to RTP networks. Activant is an investor in Gr4vy, a payments orchestrator. We also like Modern Treasury’s unified payments platform that includes connections to FedNow and other RTP networks.

- Open Banking APIs were an important catalyst in the proliferation of real-time payments. Tink (acquired by Visa), TrueLayer, Yapily, Salt Edge and other cloud-native aggregators helped broaden the adoption of data sharing, but ultimately these aggregators are not payments companies. These players lead in account information services, but they are not the ones responsible for real money movement.

- Embedded Finance applications also stand to benefit from connections to RTP networks. Many B2B transactions are financed through some form of credit (lease, term loan, or revolving facility). The Equipment Leasing & Finance Foundation reported that ~62.5% of equipment and software investment volume in 2022 was financed (or ~81.5% if credit cards were included).23 Immediate settlement would save the payors interest charges on outstanding balances, potentially increasing the volume and frequency of embedded finance transactions. Activant is an investor in Vartana, and companies like Two would likely also be net beneficiaries of this improved payment method.

Conclusion

We are confident that RTP offers a step-function increase in benefits over traditional payment options (ACH, card, and wire) and will grow to become the preferred solution in markets around the world. This transformation will likely continue primarily in domestic markets in the short term but will really take off when cross-border payments can be remitted on RTP networks connecting the world’s major payment corridors. Infrastructure players connecting FIs to RTP networks are essential enablers, and a host of new companies providing overlay services will rise to prominence. We are excited about the opportunities that this transformation will create.

If our work resonates, if you’re building in the space, or if you have a different perspective, please reach out!

Footnotes

-

Arf, Global Cross-Border Payment Flows: Current Landscape; 2023 ↩

-

UBS, Payments, Processors, and Fintech, 2022 ↩

-

McKinsey, Global Payments Map, 2023 ↩

-

Ibid ↩

-

ibid ↩

-

HSBC Global Research for transaction fees for Wise (65bp); Nerdwallet, Wire Transfers that Banks Charge (450bp) ↩

-

Matt Brown, Payfac in 1,000 Words, 2024 ↩

-

CTM File, Real-time payments pioneer, Japan shaking off cash by embracing digital payments, 2023 ↩

-

ACI Worldwide, 2023 ↩

-

ibid ↩

-

Razorpay, Unified Payments Interace (UPI): Meaning and How it works, 2023 ↩

-

ACI Worldwide, 2023 ↩

-

McKinsey Global Payments Report, 2023 ↩

-

ACI Worldwide, 2023 ↩

-

McKinsey Global Payments Report, 2023 ↩

-

ibid ↩

-

ibid ↩

-

The White House, Update on the US Strategy for addressing the root cause of migration in South America, 2023 ↩

-

GoCardless, ACH Fees - How much does ACH Cost, 2023 ↩

-

TCH, Immediate Cross-Border Payments (IXB) Pilot Set to Revolutionize International Payments, 2022 ↩

-

Midigator, The Year in Chargebacks, 2022 ↩

-

The Federal Reserve, Federal Reserve Payments Study, 2019 ↩

-

Equipment Leasing & Finance Foundation, 2022 Equipment Leasing & Finance Industry Report, 2022 ↩

Disclaimer: The information contained herein is provided for informational purposes only and should not be construed as investment advice. The opinions, views, forecasts, performance, estimates, etc. expressed herein are subject to change without notice. Certain statements contained herein reflect the subjective views and opinions of Activant. Past performance is not indicative of future results. No representation is made that any investment will or is likely to achieve its objectives. All investments involve risk and may result in loss. This newsletter does not constitute an offer to sell or a solicitation of an offer to buy any security. Activant does not provide tax or legal advice and you are encouraged to seek the advice of a tax or legal professional regarding your individual circumstances.

This content may not under any circumstances be relied upon when making a decision to invest in any fund or investment, including those managed by Activant. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Activant. While taken from sources believed to be reliable, Activant has not independently verified such information and makes no representations about the current or enduring accuracy of the information or its appropriateness for a given situation.

Activant does not solicit or make its services available to the public. The content provided herein may include information regarding past and/or present portfolio companies or investments managed by Activant, its affiliates and/or personnel. References to specific companies are for illustrative purposes only and do not necessarily reflect Activant investments. It should not be assumed that investments made in the future will have similar characteristics. Please see "full list of investments" at activantcapital.com/companies/ for a full list of investments. Any portfolio companies discussed herein should not be assumed to have been profitable. Certain information herein constitutes "forward-looking statements." All forward-looking statements represent only the intent and belief of Activant as of the date such statements were made. None of Activant or any of its affiliates (i) assumes any responsibility for the accuracy and completeness of any forward-looking statements or (ii) undertakes any obligation to disseminate any updates or revisions to any forward-looking statement contained herein to reflect any change in their expectation with regard thereto or any change in events, conditions or circumstances on which any such statement is based. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking statements.