Automation — April 1, 2025

Breaking Ground

Addressing Construction's Productivity Challenge

From skyscrapers to bridges, construction is responsible for building the infrastructure that underpins modern society. The industry makes up 14% of global GDP and is expected to have a global spend of $15 trillion in 2030.12 The task seems simple enough: build under budget, on schedule, and safely. However, construction workflows are highly inefficient and outdated. We believe this is strongly correlated to the fact that midsize construction companies allocate only 1.4% of their revenue to IT, a stark contrast to industries like industrial manufacturing that spends 2.3% and utilities that spends around 4.2%.3

But it’s not all doom and gloom. This highly complex and dynamic industry also presents a significant opportunity. Global building floor space is on track to double by 2060 – the equivalent of adding an entire New York City every month for 40 years.4 Meeting this surging demand for infrastructure and housing, amid chronic labor shortages (in developed markets) and rising cost pressures, will require a technological revolution in construction. Construction Technology (ConTech) startups looking to shake up the status quo are slowly gaining traction. These innovative companies offer digital tools, software, and solutions to address the major challenges faced by construction companies seeking to modernize and harness technology to dramatically improve efficiency.

Construction’s Productivity Woes

The construction industry has been caught in a productivity rut. From 2000 to 2022 productivity in the industry improved by only 10%, while the broader economy saw a 50% gain and the manufacturing sector delivered a 90% improvement.5 We believe that there are four key challenges underpinning this poor productivity performance:

- Construction has a fragmented ecosystem that makes unified tech adoption challenging. There are multiple stakeholders (contractors, subcontractors, suppliers, architects, engineers, clients) involved in each project and it is often difficult to relay information from one party to the next. Miscommunication and poor project data accounts for 48% of all rework on U.S. construction job sites, costing the industry over $31 billion annually.6

- The ageing construction workforce has historically been resistant to changing established analog processes. Research shows that 45% of construction workers are over the age of 45 and that these old school leaders are risk-averse and hesitant to embrace new technology and the inevitable implementation challenges that typically arise.7

- This is compounded by the lack of spending on technology in the industry. We noted above that the industry only spends an average of 1.4% of revenue on technology; manual data collection and data entry are still common on construction sites, despite increased stakeholder pressure for data transparency, integration and real-time decision-making.

- Industry margins are tight, particularly for the smaller contractors in the long tail where ~68% of businesses have fewer than five employees.8 Construction material price increases of 11.2% in 2023 and 10.3% in 2022 have eaten into profit margins and increased the pressure to remain competitive.9 The shortage of skilled workers, particularly in the residential sector where attrition rates are higher and 90% of U.S. construction companies claim to be unable to find sufficient skilled workers, has driven up the cost of labor.10 Additional pressure on margins has been driven by supply chain disruptions that have become all too common over the past few years, with an estimated ~75% of projects finishing over time and over budget.11

Despite these challenges, and in many cases specifically to address them, change is coming. Evolving industry dynamics are forcing the construction industry to lean into tech adoption. This transition is being supported by:

- Regulation and government funding in place to support ConTech: There are currently many challenges to historical U.S. government funding allocations, but the Infrastructure Investment and Jobs Act (IIJA) allocated $100 million to ConTech over the next five years.12 Additionally, the Advanced Digital Construction Management Systems (ADCMS) Grant Program, administered by the Federal Highway Administration, offers up to $5 million in grants. Similar regulations have also been introduced in Europe to incentivize or mandate the use of ConTech tools. These include the UK’s new Building Safety Act which mandates a digital “golden thread” of building data for new projects, and Sweden’s ID06 system which now requires digital IDs for all construction workers on site.

- Client demand**:** Activant’s expert interviews highlighted that there is almost always some sort of mandate for technology from the client side. Requests-for-proposals (RFPs) often specifically require a description of the use of technology when bids are submitted, and almost every project has a mandate to use a web-based project management platform.

- Increased competition in the market**:** Innovation and digital tools give contractors a competitive edge in the field and in the tender process. Experts estimate that construction companies investing in digitization and embracing new materials and advanced automation could see a 50%-60% increase in their overall productivity.13 This could be a huge competitive differentiator.

- Changing management landscape**:** The retirement of experienced construction workers is accelerating the industry’s embrace of technology. Younger, tech-savvy generations are more open to digital tools and have seen how solutions such as Procore have been able to add real value. Digital transformation is now a priority for 72% of construction companies worldwide.14

While these tailwinds are increasing technology adoption, the process is slow and there is a long way to go. We are, however, optimistic that the industry has recognized the need for change and the impact that digital tools can deliver.

Unlocking the Next Big Opportunity

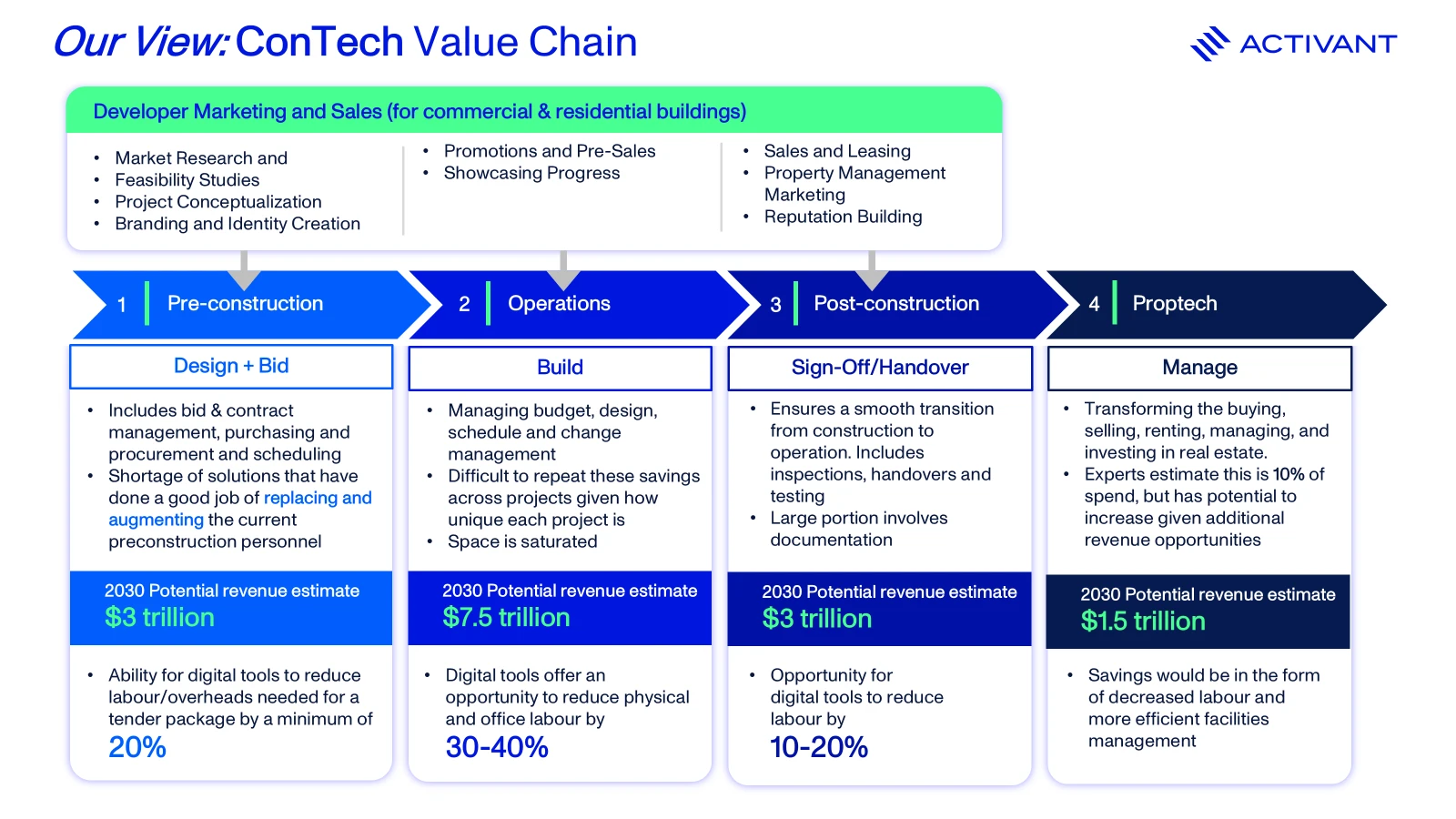

To get a better understanding of the improvement opportunities and potential profit pools available to players, as well as which customer needs were not being met, we mapped out a simple value chain and looked at each of the major phases. Our analysis suggests that there is an opportunity to deliver savings of ~20%-25% in this $15 trillion industry.15

Operations represents the largest segment in the value chain with an estimated $7.5 trillion in revenues in 2030. It is also the segment with the largest estimated improvement potential. Average gross margins in the construction industry are reported to be approximately 25%.16 If labor costs make up 30%-40% of total costs and companies can capture 80% of the estimated improvement potential of 30%-40%, this could expand gross margins to 32%-37%.17 While we don’t imagine that all these benefits would accrue to the operators, this represents an opportunity of $525 - $900 billion in 2030.The operations segment of the market is very competitive and, given the size of the value at stake, it has also attracted the greatest number of start-ups and investment.

Pre-construction and post-construction are both estimated to be $3 trillion markets in 2030, with the opportunity to improve productivity by as much as 20%. Again, if labor represents ~30%-40% of pre- and post-construction costs and if operators can capture 80% of the estimated 10%-20% productivity improvement, this could be worth between $68 billion and $180 billion. The bottom-line impact of these kinds of improvements is massive, potentially expanding the estimated industry gross margin by as much as 25%. There are a limited number of startups currently targeting these opportunities, particularly in the post-construction segment.

As the construction industry adopts more software tools, a new challenge has emerged – the fragmentation of data across apps and platforms. A contractor might use one tool for project management, another for accounting, one for Building Information Modelling (BIM), and yet others for field tracking. This inevitably leads to duplicate data entry and siloed insights. The industry currently lacks a common data standard, making integration between tools tricky and often ad-hoc. This presents a significant opportunity for the orchestration of the myriad solutions into a single, coherent workflow-sharing common data***.*** Orchestration software solutions are often the fastest growing segments within vertical markets, and ConTech is no different. The middleware connecting point solutions and synchronizing data across disparate apps and tools is the glue binding everything together. The alternative is a comprehensive end-to-end solution or unified platform that offers a suite of integrated modules. Experience in other vertical markets suggests that orchestration is a more viable solution than end-to-end suites, but some of the most successful solutions in the market today — like Access Coins ERP and Ingenious Build — are end-to-end suites.

“You can't fix what you can't measure. There's a reason why industry-leading contractors are growing so quickly - they're actually using their data to run their businesses better.”

Playing Catch-Up with the Aid of ConTech

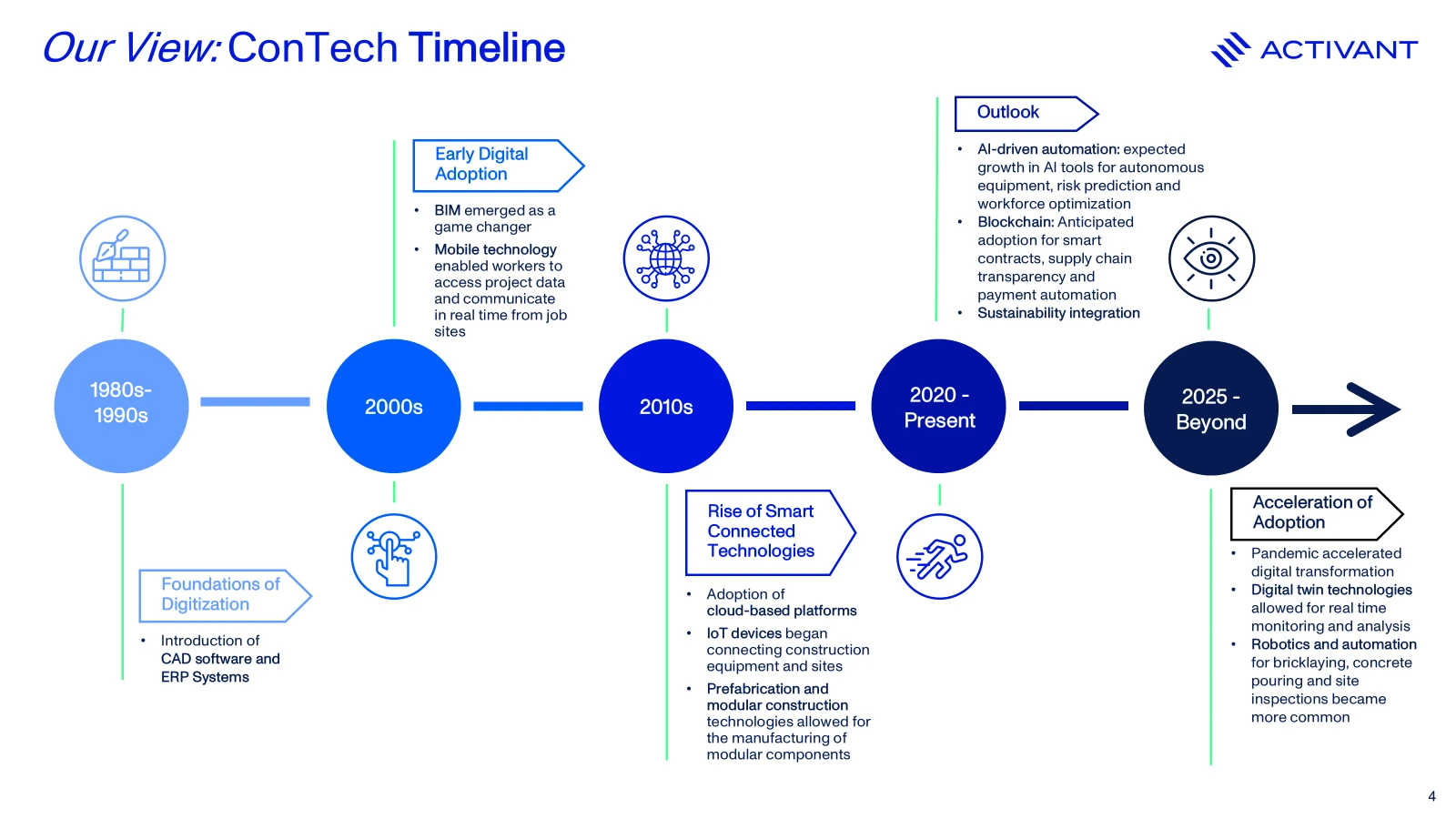

ConTech tools have achieved some major milestones over the past few years, but project management systems and BIM solutions are the only ones to have achieved large-scale adoption. The timeline below highlights the implementation of key construction technologies and their relevant impact upon the industry.

An estimated $50 billion was invested in architecture, engineering and construction (AEC) tech between 2020 and 2022, showing an 85% increase over the previous three years.18 During the same period, the number of deals in the industry increased by 30%.19 These are very positive signs, and experts highlight that many large general contractors, specifically the top 25, have established innovation teams and venture capital arms that specifically focus on ConTech solutions. Savvy investors who recognize the untapped potential and persistent market inefficiencies in construction stand to benefit from one of the last undigitized frontiers being brought online.

In 2020, ConTech represented just 0.6% of VC investment, but despite a poor year in 2023 its share had doubled to ~1.1%.20 That is tiny relative to construction’s economic weight, suggesting substantial headroom as the industry digitizes.

How We See the Market

While the first wave of ConTech focused on obvious problems like digitizing blueprints or coordinating big contractors, the next wave is attacking deeper inefficiencies and niche verticals within construction. We believe that the most promising opportunities lie in the less-glamorous back-office processes or in the long tail of users that have been overlooked.

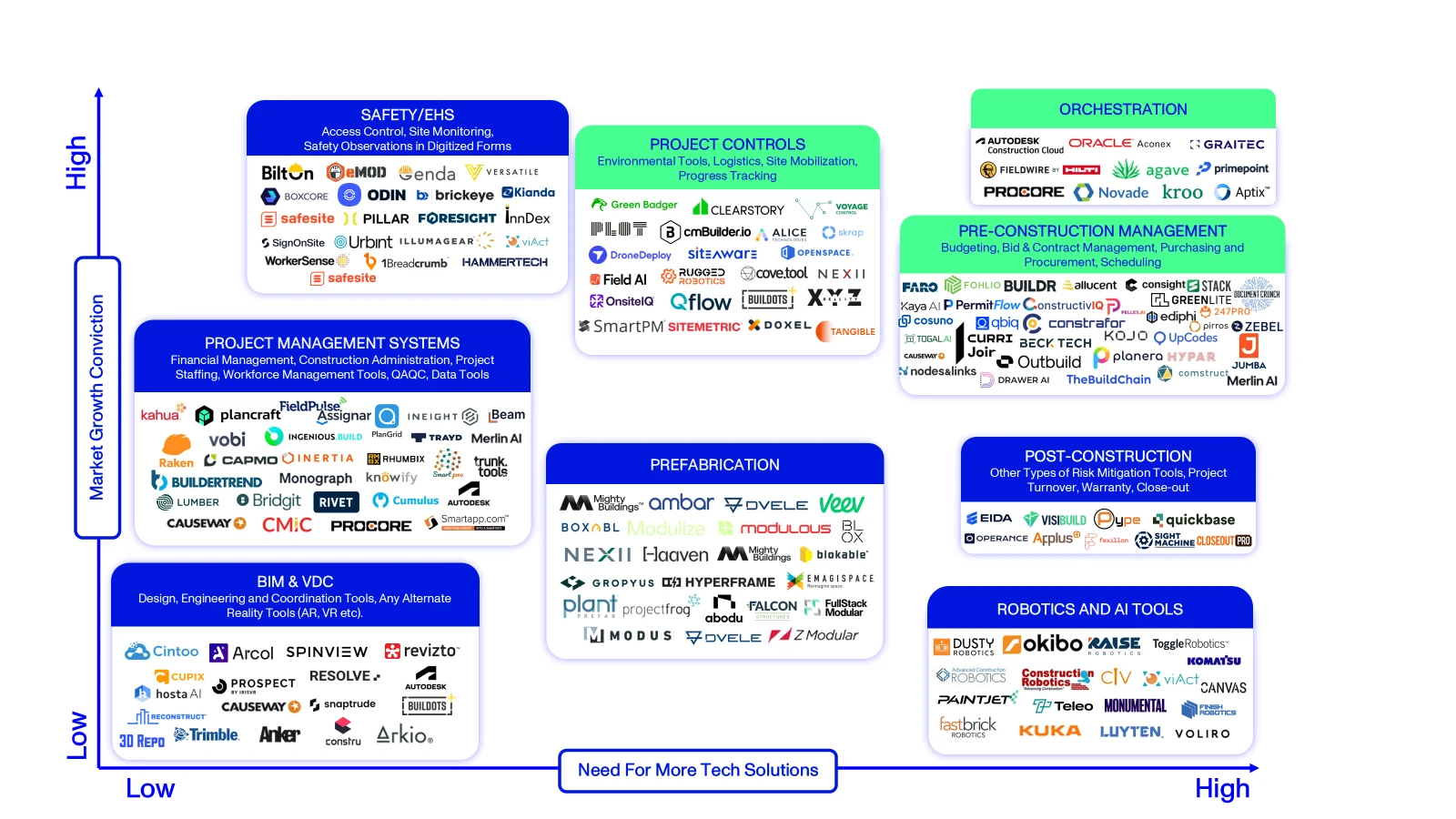

To help understand the opportunity, we arrayed the segment-specific tools and solutions on a market map with our assessment of the need for tech solutions on the horizontal axis, and our conviction in market growth on the vertical axis.

We are most excited about the opportunities in the orchestration, pre-construction, and project controls segments but there are naturally opportunities across the market.

Orchestration

ConTech orchestration refers to the integration, coordination, and automation of various ConTech tools and platforms to optimize construction workflows. It ensures seamless data flow across different software solutions, IoT devices, AI-driven analytics, and project management tools, eliminating inefficiencies and reducing project delays. The construction industry is defined by an array of point solutions. As a result, the average construction project uses multiple software tools (e.g. Procore, Autodesk, Viewpoint, Smartsheet, BIM 360, and accounting systems). These tools often don’t communicate seamlessly, causing data duplications, manual entry errors and lost information. It is estimated that in 2020 bad construction data caused $1.8 trillion in losses worldwide and was potentially responsible for 14% of avoidable rework, amounting to $88 billion in costs.21

The need for orchestrators is evident. We’re excited about players like Agave, who provide a unified API for data access across various construction software platforms. Agave’s API integrates with over 2000 companies. Kroo is a modern data management solution for construction. Contractors run their businesses 10x better with data-driven insights powered by Kroo’s turnkey data infrastructure connecting construction data silos. Their software is used on over 3,000 construction projects exceeding $10 billion in value.

“Each disconnected system means siloed data, duplicated work, and costly errors. Orchestration tools integrate a company's existing systems, automating data-sharing and ensuring teams always have accurate, real-time data no matter which app they're using day to day.”

Pre-Construction Management

This involves activities that ensure a project is well-defined, financially viable, and logistically feasible to reduce risks, control costs, and enhance efficiency. There is innovation taking place in all components of this sub-sector. AI-driven cost estimation is making bidding and budgeting faster and more accurate, eliminating guesswork. Automated design coordination and clash detection in BIM ensures errors are caught before construction begins, preventing costly rework. Predictive analytics are being used to assess risks and optimize schedules, improving project forecasting. Meanwhile, real-time collaboration platforms are breaking down silos, allowing stakeholders to make data-driven decisions earlier.

Within this space we are particularly excited about procurement tools. The construction supply chain is highly fragmented, with thousands of distributors, varying prices, and frequent materials shortages or delays. Most contractors still source materials via phone calls and emails, lacking transparency on pricing or availability. This inefficiency can lead to project delays and cost overruns. Comstruct is working on a platform that will allow construction companies to digitize and automate material purchasing. By leveraging Comstruct’s platform, construction companies can achieve significant efficiency gains, cost savings, and improved profitability through streamlined procurement processes.

We like what PermitFlow, a construction permit application and management platform for developers and general contractors, is doing. Users have reported reductions in permit approval times of up to 60%. The tool has a clear value proposition and ultimately does enable quicker project commencements. Planera offers a collaborative construction scheduling software that simplifies project management. By focusing on a user-centric design and fostering collaboration, Planera addresses common pain points in construction project management, setting itself apart from other solutions in the market.

Project Controls

This encompasses digital tools that help contractors gain a comprehensive understanding of every facet of the project. These tools allow for increased efficiency, reduced costs and improved project outcomes. We’re excited about this space because of the direct benefits and savings that contractors can realize. This makes it a lot easier to get traction as a startup, as the ROI is clearer than for other ConTech tools.

Our research suggests that progress tracking tools are essential, but those that are currently available fall short when rolling out. We’re looking for tools that are predictive as opposed to reactive, thus reducing the chance of human error within the construction process. Players like Alice Technologies automate scenario exploration with AI, enabling contractors to quickly find the most efficient, cost-effective, and risk-reduced path for their project.

“According to McKinsey, 98% of construction projects are over budget or behind schedule. We believe that schedule optimization is one of the most impactful ways to drive efficiency and cost savings in construction. Tools like ALICE help contractors move from reactive problem solving to predictive planning and decision-making—unlocking real ROI.”

We have included environmental tools within this category. Construction is responsible for 38% of global CO₂ emissions when accounting for buildings’ operations.22 In many cases, tools related to sustainability are nice to have rather than essential. Whilst public companies like Amazon have stringent environmental requirements for their projects, the average developer sees ESG as an extra cost rather than a value driver. Regulations around sustainability vary widely by region, leading to inconsistent adoption. Tangible’s unified software platform catalyzes the adoption of sustainable building materials by allowing real estate developers, architects, and contractors to seamlessly identify, manage, and report on products that meet their carbon, environmental, and social goals. Players like Green Badger aim to automate sustainability in the built environment. This allows contractors to save as much as $25 000 per year on LEED projects.

We like how Doxel uses AI to automate progress reporting for construction. By providing accurate and timely progress data, Doxel has enabled project teams to accelerate schedules by an average of 11% and achieve up to 30% savings on monthly cash flow. PLOT is a jobsite coordination tool combining delivery coordination and lead time management. This tool addresses common challenges in procurement and delivery workflows, an area we believe to have real prospects.

Outside of these three segments, there are a host of innovative players adding real value and delivering significant productivity improvement:

Post Construction: These tools are essential for transitioning a site from the construction phase to a finished, occupiable state. There are not a lot of players offering solutions in this space and the need for tools is growing. Whilst some project management tools offer components of this, such as closeout, a comprehensive tool that also covers issues such as warranty is difficult to come by.

Tools that facilitate the creation and management of detailed as-built drawings, operation manuals, and warranty information ensure a smooth and accurate transfer of knowledge from the construction team to the building owner. This helps with a smooth handover and prevents delays.

- Fexillon’s platform gives a complete overview of all build information, creating a golden thread of information and an approved digital building record at handover.

- Visibuild covers the end-to-end quality assurance management process. With 10%-15% of profits spent on post-completion defects, contractors are in serious need of tools that can ensure a smooth handover.23

Robotics & AI Tools: McKinsey estimates that AI could boost construction productivity by up to 20% by enabling better project planning and resource management.24 The demand for AI-powered construction solutions is expected to grow to $5 billion by 2030.25 There are lots of innovative players within this segment.

- Dusty Robotics develops robot-powered tools for the modern construction workforce. Their flagship product, the FieldPrinter, turns digital BIM designs into fully constructible layouts in the field quickly and accurately.

- Canvas is a construction robotics company that uses machine learning to install drywall at construction sites. It delivers unrivalled quality, speed, and predictability by putting robots in the hands of skilled workers. We like that both tools are reducing the need for manual labor and thus addressing a key pain point in the construction industry.

Safety/EHS: The construction industry accounts for ~20% of all deaths among US workers, the highest of any sector.26 Companies using AI-driven safety tools have seen a reduction in workplace accidents by as much as 25%, resulting in fewer injuries and lower insurance costs.27

- Brickeye distinguishes itself from other construction safety tools through their comprehensive, IoT-enabled platform that integrates advanced monitoring, real-time data analytics, and intelligent automation to enhance job site safety and productivity.

- Odin has a fully integrated approach to workforce risk management, offering a suite of features designed to enhance safety, compliance, and operational efficiency on large-scale job sites.

Prefabrication: McKinsey analysis suggests that modular techniques could allow home builders to accelerate end-to-end project timelines by 20 to 50 percent while reducing costs by up to 20 percent.28

- Haaven’s platform brings together all the right skills from architects, prefabricated home builders and contractors to help bring people’s homes to life.

- Modulize is an offsite construction (OSC) platform powered by calculation and design automation.

Project Management Systems: These tools are the bread and butter of every contractor. Project management systems are viewed by industry insiders as an essential part of the tech stack. As a result, hundreds of players have entered the market over the past few years, making these tools highly commoditized. Project management tools like Procore, PlanGrid or Buildertrend streamline communication and centralize project data, helping all stakeholders stay aligned.

- Trunk Tools has developed a suite of AI agents designed to automate tedious tasks, improve communication, and make construction projects more efficient and predictable. Its platform organizes unstructured project data, ensuring critical information is available, thereby reducing delays.

- Inertia is a construction management platform that provides solutions to alleviate jobsite productivity challenges. The tool integrates seamlessly with Procore and offers intelligent asset tracking by centralizing all Procore activities and workflows. Given how widely used Procore is, this feature acts as a competitive advantage that will allow scale.

BIM & VDC: BIM – essentially 3D digital blueprints enriched with data – has become mainstream in design and is now extending through construction and into operations. These were some of the earliest adopted tech solutions in the construction sector. As a result, today this is a difficult market with lots of competitors and tech saturation. BIM allows all stakeholders to collaborate around a single source of truth for the project, reducing errors from working off outdated plans. Startups and incumbents are building on BIM with cloud-based collaboration platforms that connect the office and field. Newer entrants are also targeting specific gaps: field connectivity (bringing digital tools to the jobsite via rugged tablets and mobile apps), supply chain visibility (material tracking from factory to site), and digital twins (real-time digital replicas of jobsite conditions, updated via IoT sensors and drones). AR/VR Tools such as HoloBuilder and IrisVR can visually demonstrate the value of tech to stakeholders, making the benefits more tangible and engaging. BIM tools also significantly enhance data transparency and integration in construction projects.

- Snaptrude is a collaborative cloud-based building design platform for architects and interior designers. This accelerates their concept design workflows, solving for a real pain point.

- Buildots has created an AI-powered progress tracking tool that accurately measures site performance and reduces delays by up to 50%.

Big Opportunities Lie Ahead

The construction industry is poised for a digital revolution. Despite facing the persistent challenges of a fragmented ecosystem, an ageing workforce, lack of spending on technology, and tight industry margins, the tide is turning, and increased investment is driving the adoption of ConTech. While adoption has been uneven, with segments like project management and BIM leading the way, significant opportunities remain. Government support, client demand, increased competition in the market, and a generational shift in the management landscape are further accelerating this transformation. Increased investment underscores the industry’s recognition of ConTech’s potential to address the productivity challenge that has plagued the industry for years.

Importantly, the narrative is no longer just theoretical. Over the last few years, we’ve seen a surge of startup activity, venture funding, and real adoption that validates this thesis. ConTech is transforming from a niche backwater to a vibrant ecosystem of companies attacking every piece of the value chain.

Footnotes

-

Gartner, IT Key Metrics Data 2023: Industry Measures — Insights for Midsize Enterprises, 2022 ↩

-

World Economic Forum, As construction accelerates globally, implementing sustainable building practices is critical, 2024 ↩

-

McKinsey, Delivering on construction productivity is no longer optional, 2024 ↩

-

PR Newswire, New Research from PlanGrid and FMI Identifies Factors Costing the Construction Industry More Than $177 Billion Annually, 2018 ↩

-

Construction Dive, Construction’s age problem: A foreboding exodus of experience, 2023 ↩

-

Ooma, Which industries have the highest percentage of small businesses?, 2025 ↩

-

DDC Solutions, How Rising Costs Are Reshaping the Construction Industry and What Business Owners Can Do About It, 2025 ↩

-

Construction Dive, Infrastructure bill contains $100M for construction technology, 2021 ↩

-

For Construction Pros, Construction Digitization: Understanding the Impact on Profitability, 2021 ↩

-

RICS, Connected construction: Industry digitalisation in numbers, 2020 ↩

-

Ready Ratios, Building Construction General Contractors And Operative Builders: Average Industry Financial Ratios for U.S. Listed Companies, 2023 ↩

-

Based on multiple sources such as: cost breakdowns from Turner Construction, RSMeans Data, Expert calls ↩

-

McKinsey, From start-up to scale-up: Accelerating growth in construction technology, 2023 ↩

-

Construction Dive, ConTech funding plummets in 2023, despite more deals, 2024 ↩

-

MSuite, Bad Construction Data Costs Industry $1.8 Trillion Worldwide, 2022 ↩

-

Plan Be Eco, Carbon footprint in the construction industry: meaning, challenges and the future, 2024 ↩

-

Visibuild, The benchmark for construction quality management, 2025 ↩

-

Construction Today, The Rise of Artificial Intelligence in Construction, 2024 ↩

-

Globe Newswire, Artificial Intelligence (AI) in Construction Market, 2022 ↩

-

US Bureau of Labour Statistics, Injuries, Illnesses and Fatalities, 2020 ↩

-

Construction Today, The Rise of Artificial Intelligence in Construction, 2024 ↩

Disclaimer: The information contained herein is provided for informational purposes only and should not be construed as investment advice. The opinions, views, forecasts, performance, estimates, etc. expressed herein are subject to change without notice. Certain statements contained herein reflect the subjective views and opinions of Activant. Past performance is not indicative of future results. No representation is made that any investment will or is likely to achieve its objectives. All investments involve risk and may result in loss. This newsletter does not constitute an offer to sell or a solicitation of an offer to buy any security. Activant does not provide tax or legal advice and you are encouraged to seek the advice of a tax or legal professional regarding your individual circumstances.

This content may not under any circumstances be relied upon when making a decision to invest in any fund or investment, including those managed by Activant. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Activant. While taken from sources believed to be reliable, Activant has not independently verified such information and makes no representations about the current or enduring accuracy of the information or its appropriateness for a given situation.

Activant does not solicit or make its services available to the public. The content provided herein may include information regarding past and/or present portfolio companies or investments managed by Activant, its affiliates and/or personnel. References to specific companies are for illustrative purposes only and do not necessarily reflect Activant investments. It should not be assumed that investments made in the future will have similar characteristics. Please see "full list of investments" at activantcapital.com/companies/ for a full list of investments. Any portfolio companies discussed herein should not be assumed to have been profitable. Certain information herein constitutes "forward-looking statements." All forward-looking statements represent only the intent and belief of Activant as of the date such statements were made. None of Activant or any of its affiliates (i) assumes any responsibility for the accuracy and completeness of any forward-looking statements or (ii) undertakes any obligation to disseminate any updates or revisions to any forward-looking statement contained herein to reflect any change in their expectation with regard thereto or any change in events, conditions or circumstances on which any such statement is based. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking statements.