B2B Commerce — February 24, 2026

Stablecoins: Enabling Direct Flights

How stablecoins are cutting payment’s layovers and streamline treasury operations

Cross‑border payments are a critical pillar of the global financial system, underpinning international trade, investment, remittances, and other capital flows totaling tens of trillions of dollars each year. However, this area has not improved as quickly as other parts of finance. That is starting to change, as stablecoins are now moving from the outer margins of the crypto world into the main debate about how money moves across borders. After years of testing and a combination of mounting economic pressure, maturing technology, and clearer regulations, the discussion has shifted from if stablecoins will matter to where and how quickly they will be adopted.

A Market Ripe for Disruption

The scale of the global payments industry is sometimes difficult to comprehend. In 2024, 3.6 trillion transactions supported the flow of $2 quadrillion in funds and generated $2.5 trillion in revenue.1 Industry players earned an average return on equity of 18.9% and, while rising interest rates slowed global growth from 12% in 2023 to only 4% in 2024, the industry remains massive and highly profitable.2

It is also remarkably inefficient. This is particularly true of the $179 trillion cross-border payments market where transactions often take two to five days to settle and costs vary widely. Fees can range from below 5bps for B2B payments in well-established corridors to over 1,000bps for low volume remittances in high-cost corridors.345 Lower-value payment flows account for only about 10% of the cross-border remittances, yet contribute almost one-third of industry revenues The segment is forecast to grow at rates well above industry averages, driven by emerging market growth, greater financial inclusion, and the continued rise of e-commerce.6 Not surprisingly, it is attracting the greatest attention from new entrants offering lower costs, quicker clearing and settlement, and greater transparency.

While banks continue to dominate the large value transfer market, fintechs and neobanks like Wise and Revolut have made major inroads and grown rapidly by reducing friction and costs using smart liquidity pooling, local accounts, and software automation. We are also beginning to see the linking of local real-time payments networks, we highlighted in our 2024 report “It’s Time Local Went Global”.7 Brazil’s Pix is expanding beyond its domestic market into Latin America, India’s UPI is collaborating with Singapore’s MAS, and the Arab regional payments system Buna is flourishing across the Middle East. At the same time, stablecoins are emerging as an alternative to traditional payment rails.

Within this new “multi-rail” reality, stablecoins stand out for their potential to reshape how we think about payment flows, liquidity and treasury management, compliance reporting, and fraud detection. We are not alone in this view. Many of the biggest names in the traditional cross-border payments market — including Visa, Mastercard, J.P. Morgan Chase, Western Union, PayPal, and SWIFT — have announced major stablecoin initiatives. New players like Revolut, Stripe, Wise and Airwallex (an Activant portfolio company) are doing the same.

A Catalyst for Change?

Stablecoins — digital assets designed to maintain a stable value by pegging their worth to reserve assets such as fiat currencies like the US dollar, commodities or baskets of assets — emerged more than a decade ago when Tether tied the value of USDT to U.S. dollar reserves. Infrastructure players like Fireblocks and BVNK soon followed as the financial industry explored the potential of blockchain-powered, fiat-backed, stable value solutions for everyday banking needs.

This promising beginning was challenged with the collapse of TerraUSD (an algorithmic, non-collateralized stablecoin rather than a fiat- or asset-backed stablecoin) in 2022 and the failure of Silicon Valley Bank (SVB), where Circle had $3.3 billion of its USDC stablecoin reserves invested, in early 2023. The US government ultimately guaranteed SVB’s reserves, and the industry was able to rebuild after this period of uncertainty. The number of tokens in circulation has resumed its upward trajectory and regulatory clarity has begun to emerge. The European Union’s MiCA (Markets in Crypto-Assets) regulation, passed in June 2024, and the US GENIUS (Guiding and Establishing National Innovation for US Stablecoins) Act, passed in July 2025, have provided clearer regulatory framework for the use of stablecoins in payments, positioning the market for growth.

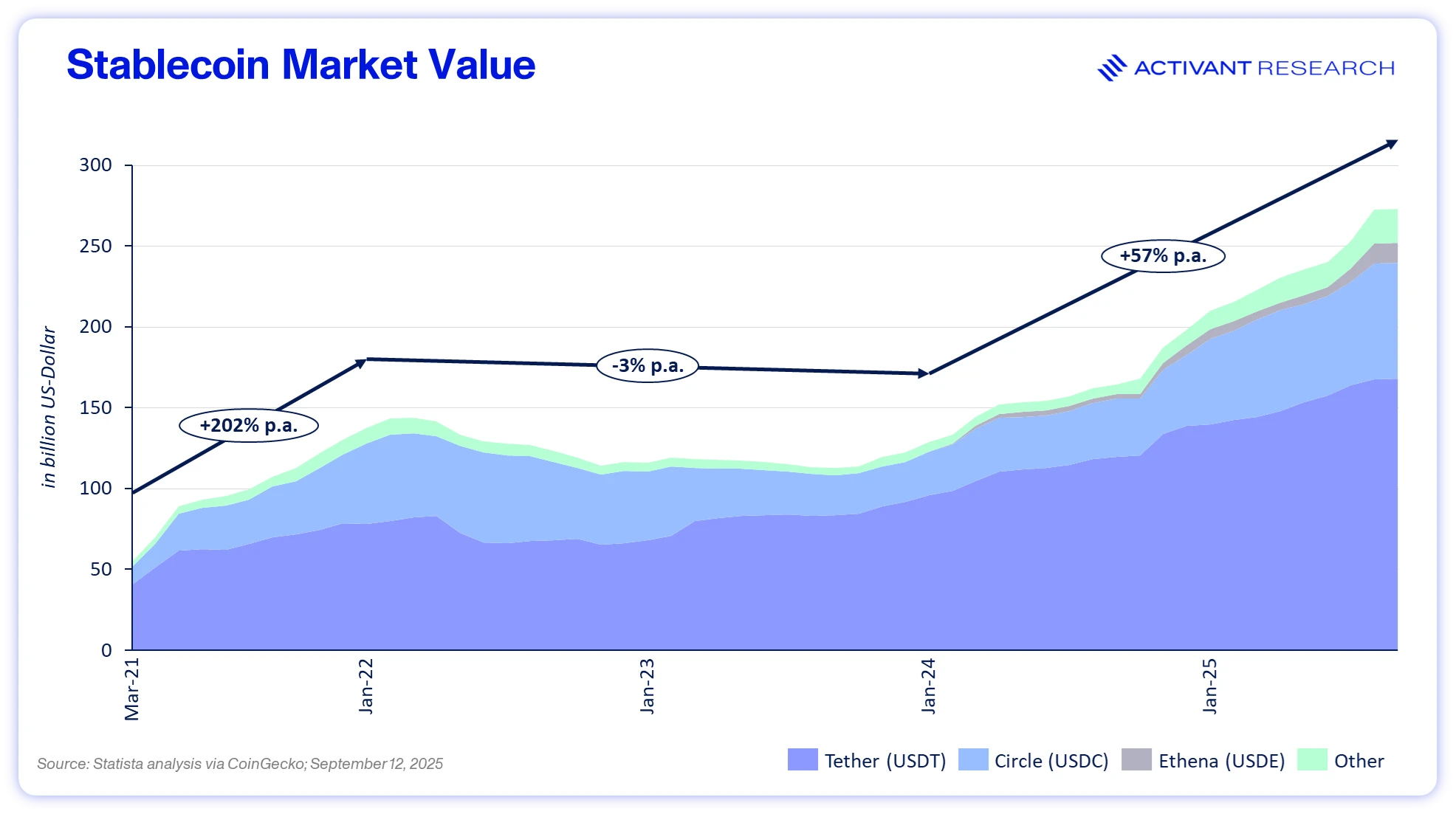

A review of the market value of the ten largest stablecoins between 2021 and 2025 illustrates this evolution clearly: an initial period of euphoria, followed by two years of stagnation , and, more recently, a renewed acceleration in growth.

The approximately $250 billion of issued stablecoins in mid-2025 only facilitated about $30 billion of transactions daily, which represents less than 3% of cross-border payments.8 Forecasts nevertheless point to substantial expansion and Citibank projects that it may grow to as much as $4.0 trillion by 2030 in their “bull case”, with their conservative “bear case” still a material 3.5x growth over the next five years to approximately $900 billion.9 Our own expectations sit between these bounds, a view shared by Standard Chartered and others.10

These forecasts are built on a series of very real advantages that stablecoins offer over the current legacy payment systems of traditional correspondent banking. Much of the current commentary focuses on cost, but this advantage may prove transitory as competitive pressure forces legacy rails to reduce fees.

“The real value of stablecoins isn’t tighter spreads, it’s eliminating float. When settlement happens in minutes instead of days, you unlock trapped capital across corridors. That shift from idle to productive capital is worth far more than a few basis points on FX.”

We agree that the more durable and transformative benefits of stablecoins lie elsewhere:

- Speed and capital efficiency: Near-instant 24/7/365 stablecoin settlements free funds that would otherwise be tied up for days, unlocking productive use of working capital and reducing pre-funding requirements.

- Programmability: Seamless integration into smart contracts enables automated payment flows, conditional logic, and direct links to treasury management and ERP systems.

- Financial inclusion: Anyone with an internet connection, smartphone and digital wallet can send and receive funds without requiring a verified bank account or access to MTO locations and services.

- Transparency: Blockchain-based reporting provides full transaction traceability, in contrast to the limited visibility of traditional flows.

- Transaction security: Digital controls and immutable ledgers enhance security, though with the caveat that transactions are irreversible and non-custodial wallet holders bear the risk of key loss or theft.

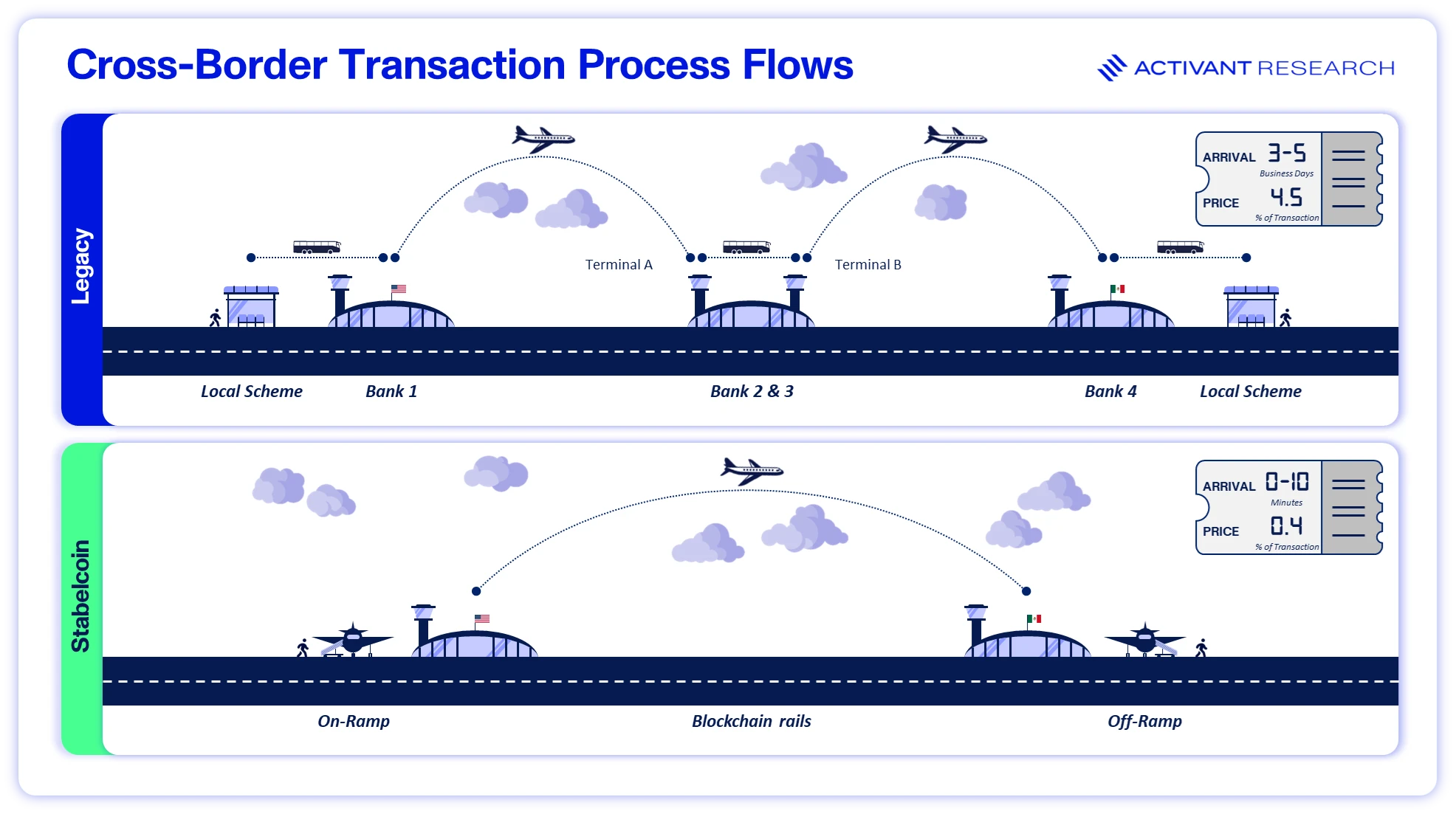

It is often said that users don’t care about stablecoins themselves but rather about the benefits they deliver. We agree and believe that those benefits are real. The simple analogy of “direct flights” in a world of layovers neatly captures the time and cost differences between legacy correspondent banking based cross-border payments and stablecoin based transfers.

If the advantages are as compelling as we have described, one might expect rapid roll-out and adoption globally. In practice, this outcome is unlikely.

The Likely Near-Term Opportunity

The airplane analogy remains useful, with one important caveat: it assumes everyone holds a stablecoin wallet and has no need to convert back to fiat. But in the world we live in today, stablecoins need to fit into the existing banking and fiat networks to be functional. While stablecoins represent a new rail to improve money movement, to drive adoption players need to work on making the shift between the stablecoin world and traditional payments seamless.

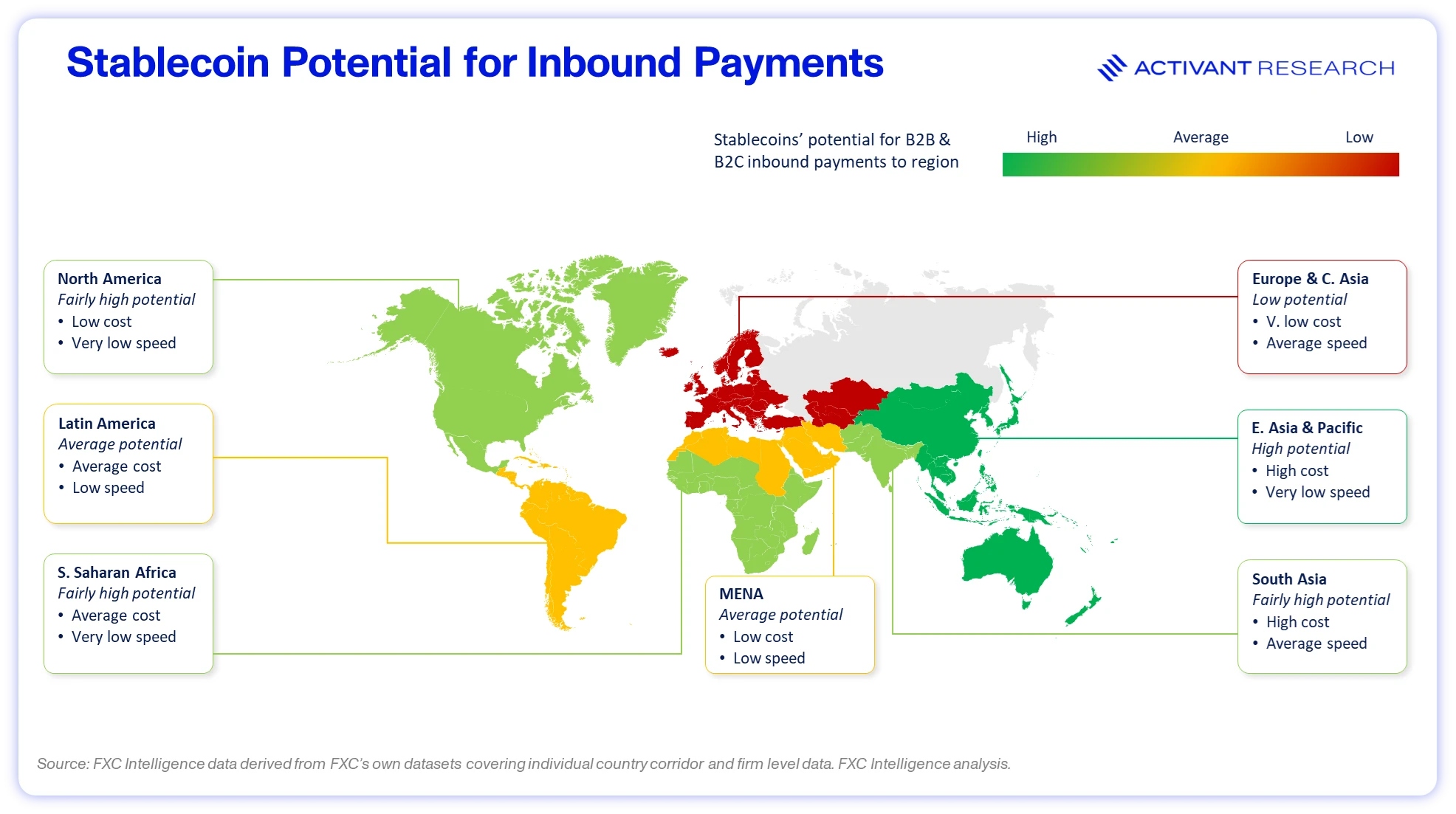

It is therefore critical to recognize that the global business (B2B and B2C) and consumer (C2B and C2C) cross-border payments markets are very different.B2B payments make up 97% of cross-border flows yet only contribute an estimated 57% of industry revenue.11 Many of these flows are in well-traded currency pairs (such as the US dollar and euro) and between established financial centers that are inherently more efficient than less developed centers and more exotic currencies. There are also very significant differences in costs and time to settle across regions. The economic case for change thus varies widely and inertia is a limiting factor that is often underestimated. FXCintelligence created a helpful chart that summarizes the estimated potential for stablecoin adoption around the world.12

It’s no surprise that stablecoins are gaining the most traction in corridors where traditional services are expensive and slow. Sub-Saharan Africa, Latin America, and parts of East Asia lead the world in stablecoin adoption for payments, reflecting the inefficient functioning of traditional payment systems.13 In Europe, by contrast, efficient domestic payment systems reduce the incentive to shift away from established rails.

Nonetheless, stablecoin payment volume has grown tenfold in the past four years, topping $27 trillion over the last year.14 A BCG analysis found that while the majority of stablecoin volume is still tied to crypto trading and decentralized finance, about 5%–10% (over $1 trillion in 2024) involved “genuine” payments such as remittances, corporate treasury transfers, and payments in high-inflation markets.15 This real-world usage is expected to surge as more businesses and individuals discover stablecoins’ utility.

Another driver of stablecoins will likely be the adoption of agentic AI. As of Q1 2024, 90% of all stablecoin volume was driven by bots, performing activities such as crypto arbitrage, liquidity provision, and market making.16 While some see this as a weakness, Velocity’s CEO Eric Queathem correctly suggests that this should be seen as evidence that AI agents will leverage stablecoins’ programmability to transact with each other over blockchain rails, rather than traditional ones.

At the same time, central banks around the world continue to experiment with digital currencies (CBDCs). These are digital versions of fiat currencies issued and regulated by central banks that aim, amongst other things, to improve cross-border payments. As of January 2026, the Bahamas was already live, with larger currencies such as the US dollar and euro remaining in concept stage. While CBDCs will likely coexist with private stablecoins over time, we believe that regulatory clarity matters far more than CBDC experimentation for driving near-term adoption.17 The introduction of comprehensive regulatory frameworks (most notably in the US and Europe) has given market participants the confidence to build and invest. Even so, there is still a long way to go, as many jurisdictions lack equivalent frameworks, and global harmonization of standards around licensing, reserve requirements and cross-border compliance remains a work in progress. As this regulatory foundation continues to develop, stablecoins have begun to emerge as a credible alternative to conventional cross-border payments infrastructure, and many incumbents are actively preparing for a material shift ahead. This shift, however, won’t happen without underlying technology and a broad ecosystem of associated solutions.

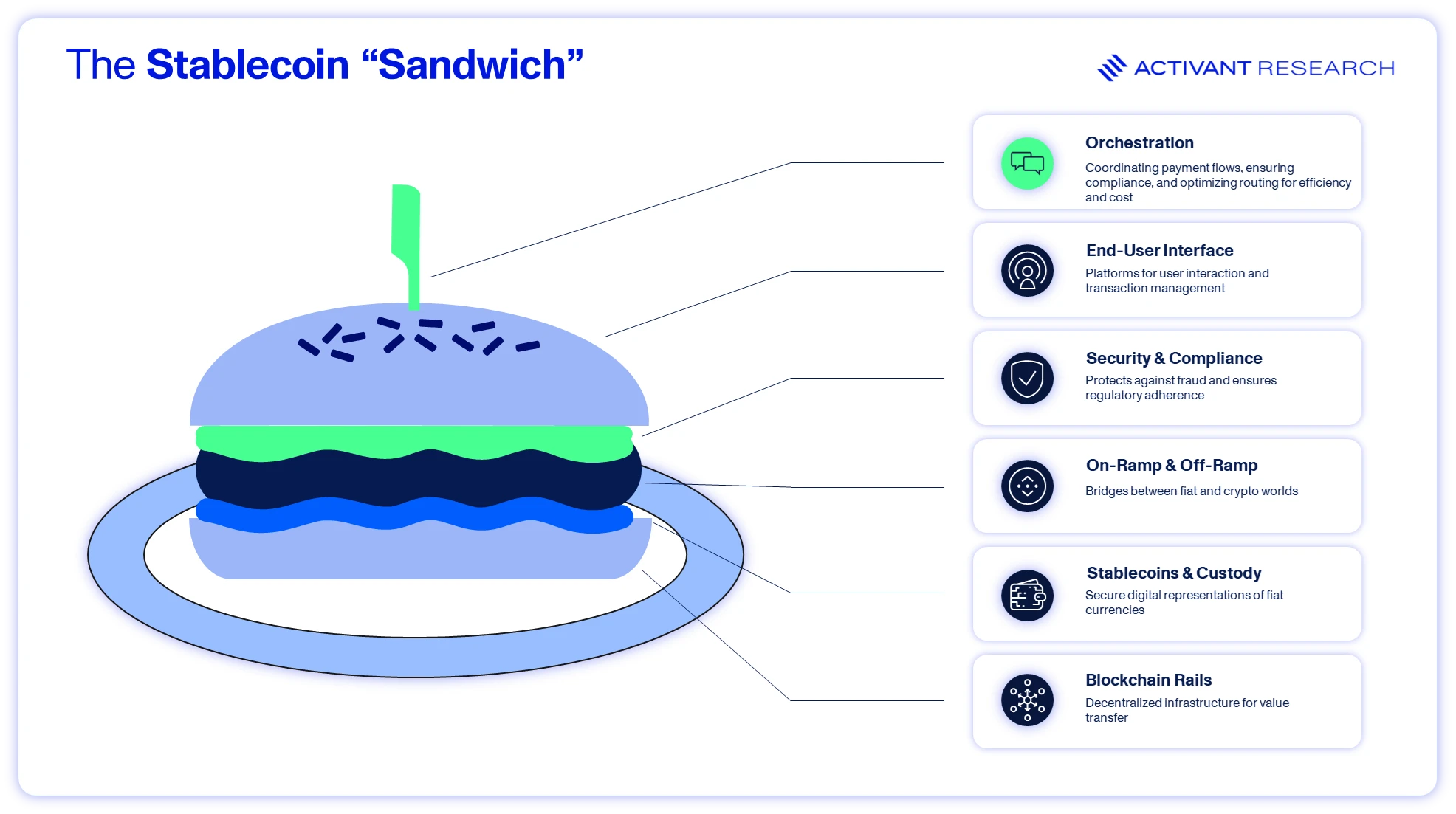

The Stablecoin Sandwich: How the Tech Gets Stacked

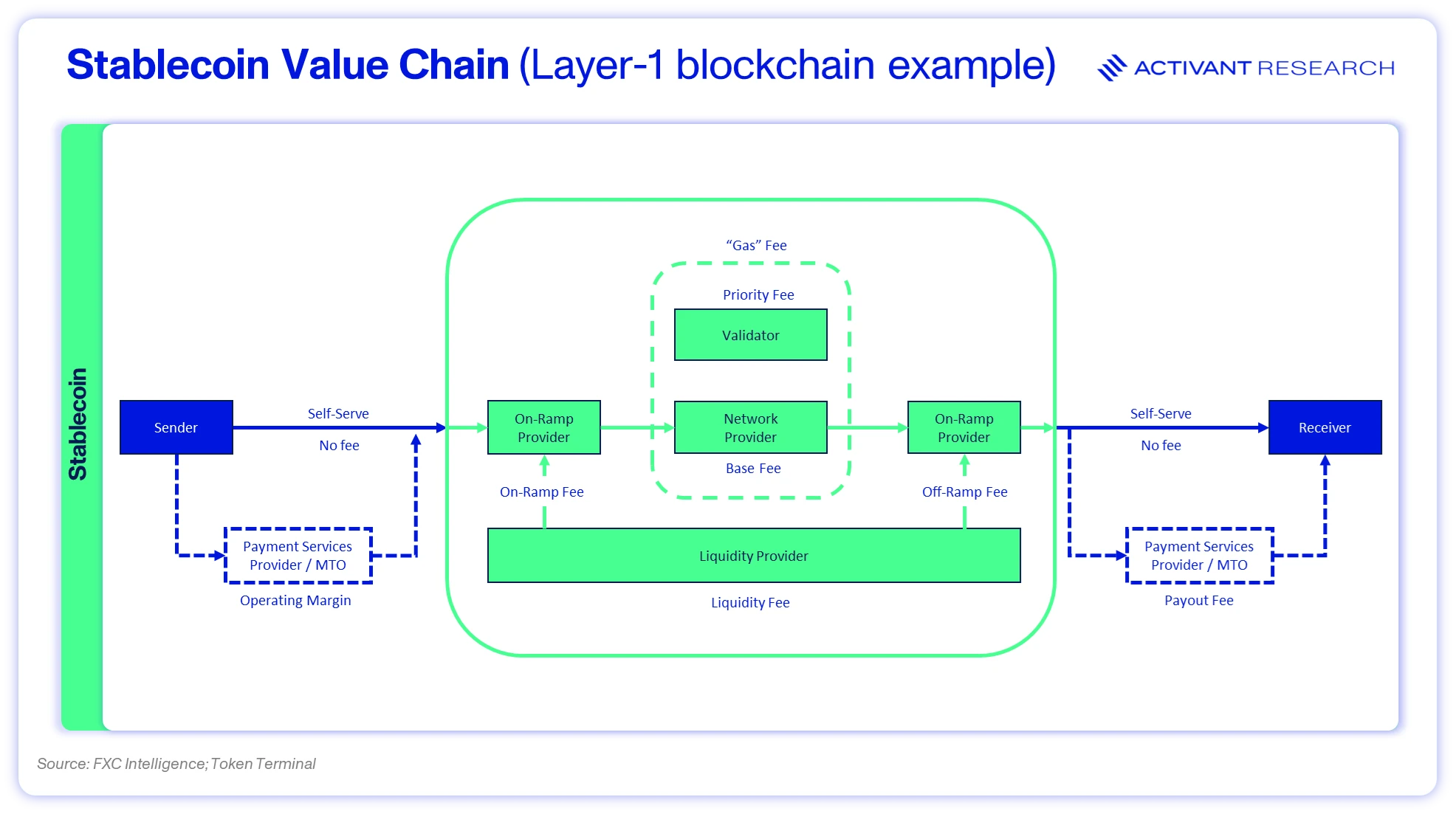

While the “direct flight” analogy captures the user experience, making it work in practice requires a complex stack of infrastructure: the “stablecoin sandwich.” In this model, fiat is converted into a stablecoin for the cross-border leg and then reconverted into fiat at the destination or stored in digital form in a wallet.

1. Orchestration Layer

Sitting on top of the stack is the orchestration layer, the intelligence that ties everything together. Orchestration providers coordinate payment flows end-to-end, determining the optimal routing across blockchains, stablecoins, liquidity providers and on-/off-ramp partners for each transaction based on cost, speed and compliance requirements. Much like users of traditional banking are unaware of how their funds move through correspondent banking networks, stablecoin orchestration abstracts away the complexity of blockchain selection, gas-fee optimization and multi-rail settlement. Providers such as Velocity (an Activant portfolio company) offer APIs and orchestration tools that enable enterprises to manage stablecoin treasury, routing and settlement across multiple blockchains and payment rails without having to build bespoke infrastructure in-house. This approach unlocks gains in the form of more productive capital. As pre-funding is eliminated, customers can get paid 24/7/365, because settlement isn’t tied to banking hours.

2. End-user Interface Layer

This is the layer customers interact with directly through mobile apps, APIs, or payment dashboards. The goal is simplicity. A migrant worker using a remittance app doesn’t care about blockchains or liquidity pools. They simply want to send $200 to Maria in Mexico as quickly and cheaply as possible and are satisfied when they see “fee: $0.50, delivery: 5 minutes” on the screen. Behind that button press, the system converts funds to a stablecoin like Tether’s USDC or Circle’s USDT, sends it over Stellar or Tron blockchains, and redeems it via a local mobile-money partner or stores it in a digital wallet as a stablecoin or fiat equivalent.

3. Security & Compliance Layer

Despite the decentralized nature of the underlying technology, compliance remains deeply centralized. Stablecoin providers must integrate robust KYC/AML, sanctions screening, smart-contract audits, and regulatory reporting. As regulatory scrutiny increases, this layer is becoming a competitive advantage rather than a burden. Trusted compliance unlocks institutional adoption.

4. On-Ramp & Off-Ramp Layer

These bridges connect the blockchain ecosystem to the fiat world. On-ramps convert local currency into stablecoins; off-ramps convert stablecoins back into cash or bank deposits. They take the form of crypto exchanges, fintech aggregators, licensed money transfer operators, or direct bank partnerships. The smoother these gateways become, the more invisible the crypto layer will feel to users. It is worth noting that at some point consumers may not actually on-ramp and off-ramp anymore, but that is not likely in the near term and the need for interoperability between fiat currencies and stablecoins will not disappear for the foreseeable future.

5. Stablecoin & Custody Layer

At the core of the stack sits the stablecoin issuers – the entities responsible for minting and redeeming tokens against fiat reserves. Tether (USDT) and Circle (USDC) are the largest players with approximately 64% and 24% of issued stablecoins respectively. There are a number of smaller players, like PayPal (PYUSD), Ripple (RLUSD), Paxos (USDG) and Stripe (USDB), but none of them represent more than 0.5% of issued stablecoins. Their job is to maintain the one-to-one peg through transparent collateral management and regular attestations. Trust in these issuers is foundational; if the peg fails, confidence in the system collapses.

6. Blockchain Rail Layer

This layer provides the transaction rail itself, the blockchain network that carries the transaction. Stablecoins operate across networks like Ethereum, Tron, Solana, or Polygon, which offer various trade-offs in cost, speed, and decentralization. Ethereum provides security but can be slow and expensive; Tron and Solana offer cheaper, faster throughput. The choice of rail determines the economics of the system. Blockchains fall broadly into two categories: Layer-1 blockchains, which form the base infrastructure, and Layer-2 blockchains, which sit atop Layer-1s to increase speed and reduce cost. Ethereum, the largest Layer-1 blockchain, forms the foundation for Arbitrum and Base, which are both able to handle a greater number of transactions per second at a fraction of the cost given their rollup architecture and compressed data transfer to the underlying Layer-1 blockchain.

This layered stack also redefines value chain economics. In traditional card payments, the issuer captures most of the value. In the stablecoin world, the equivalent (the wallet provider) earns almost nothing, and Layer-1 and Layer-2 networks are becoming increasingly commoditized as no enterprise customer asks which chain is being used to transfer value. Instead, value is migrating upward to the orchestration layer, where providers that can reliably route, settle and report across a fragmented infrastructure while meeting evolving regulatory obligations are building the most defensible positions in the ecosystem. We see this as a value chain flip.

This full stack, the stablecoin sandwich, is what enables the system to function as an integrated, compliant, user-friendly experience. With this high-level overview of the various elements of the stablecoin value chain and its shifting economics, we can now examine how these rails compare end-to-end and where the true efficiency gains begin to emerge.

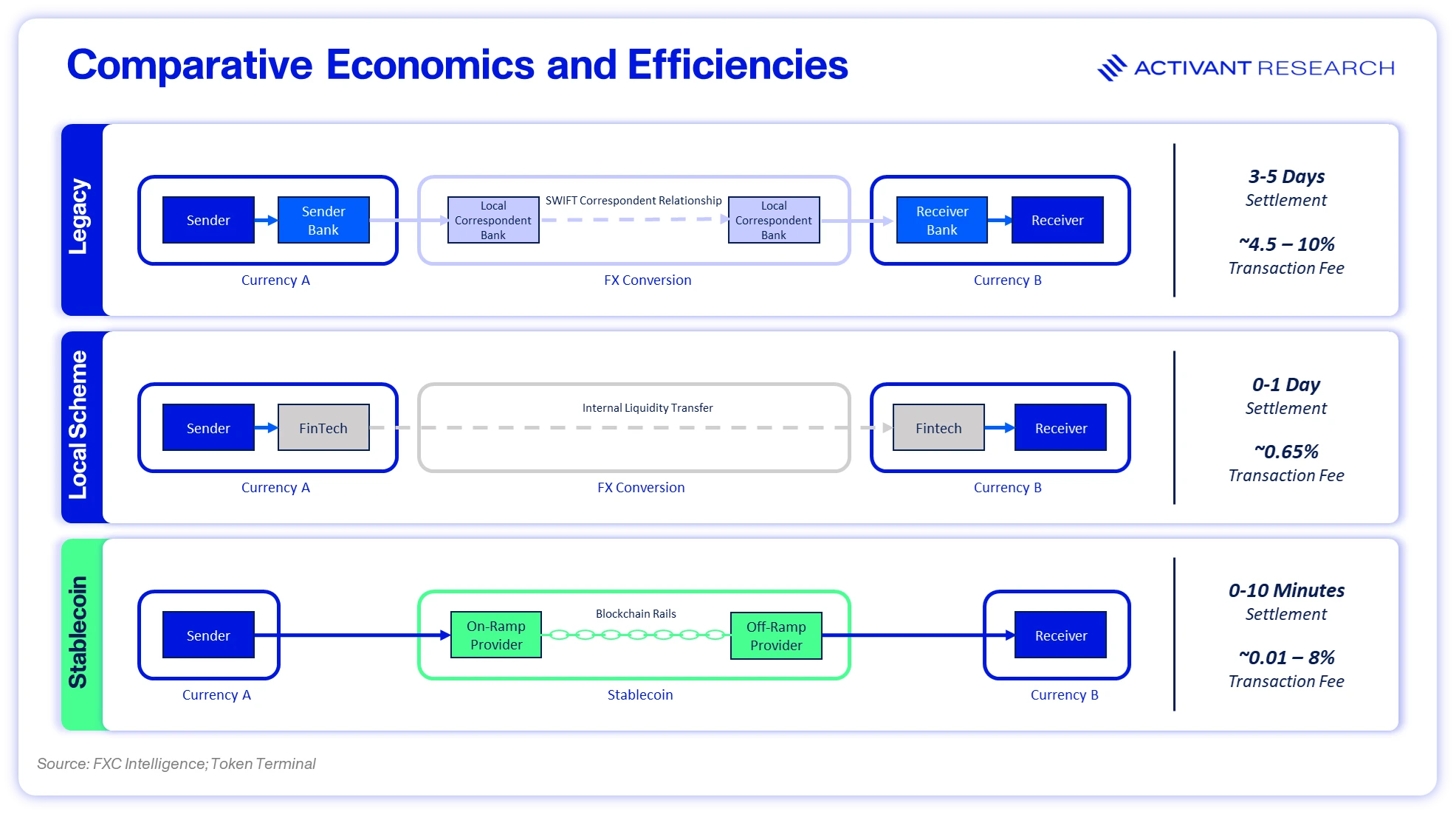

Not All Rails or Stablecoins are Equal

The “average of averages” is almost always misleading, and cross-border payments are no exception. A quick look at the exhibit below shows the incredible range in cost and efficiency between legacy correspondent banking, local access schemes, and stablecoin options.

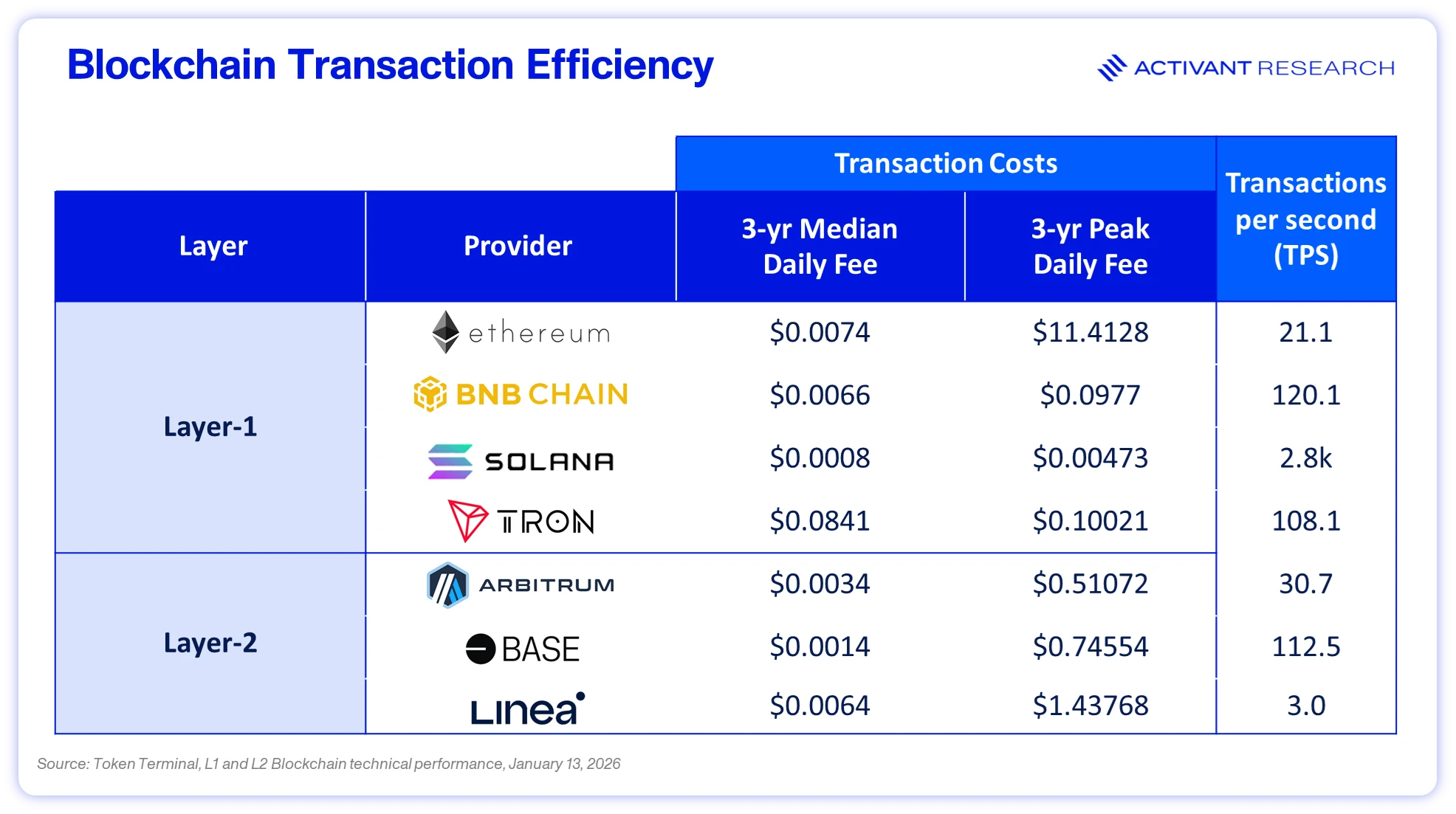

Stablecoin solutions are almost always very time efficient (assuming that there are no dependencies on fiat on-/off-ramps), but they are not always cost-effective, and prices can be highly volatile. Data from Token Terminal18 shows that while Ethereum’s average daily transaction price over the past three years was $0.134, its peak daily average was $29.58. Over the same period the median daily transaction price was $0.0074 with a peak median daily price of $13.093. The variability is striking.

Layer-2 based stablecoins offer a different profile with much lower average transaction fees despite being built on the foundation of layer-1 blockchains like Ethereum. Over the same three-year period, Arbitrum One, a layer-2 blockchain deployed over Ethereum, had an average daily transaction price of $0.0127 and a daily peak of $0.7033. The median daily transaction fee over the period was $0.0034 with a peak of $0.51072.19

The table on the next page summarizes median and peak daily transaction fees as well as the average number of transactions processed per second over the same three-year period.20 A quick glance at the data shows that Ethereum’s popularity is not based on its technical performance, but rather its widespread distribution that provides good liquidity for major stablecoins.

Importantly, the transaction costs (or fees) shown above represent only the on-chain fees that are often referred to as network or “gas” fees. There are a host of other charges and fees incurred across the entire stablecoin value chain, as the illustration below highlights.

Gas fees are typically made up of the base fee (set by the network) and priority fee (or tip) determined by the user or their wallet algorithms to expedite and move up the queue. Additional charges include the on-ramp and off-ramp fees (including fees for AML/KYC scans and FX), as well as fees for the liquidity provider that maintains stocks of the native tokens and stablecoins required to settle the gas fee payment and transfer itself. If the sender uses a payment services provider or money transfer operator (MTO) to initiate the transaction, these vendors receive compensation that is typically determined relative to the size of the transaction. Similarly, if an MTO is used to deliver the payment in fiat currency, the receiver incurs a service charge. Senders and receivers can avoid charges by self-serving via apps or digital wallets.

Layer-2 blockchains (that sit on top of layer-1 blockchains) naturally have a slightly more complicated cost structure. The execution fee includes a layer-1 gas fee for the underlying blockchain and a sequencer fee to cover the costs of the entity handling the transaction. Despite this, the fact that layer-2 blockchains bundle transactions result in lower costs.

The net result of the more complicated cost structure of blockchain transactions is that they may be cheaper than legacy and local schemes, but the pricing is highly variable. This reinforces the strength of the orchestration layer sitting on top of the stablecoin stack. By abstracting complexity via smart routing orchestration platforms can always select the most cost-efficient solution, choosing between different stablecoin and fiat rails. If time is important or you are transferring in exotic currency pairs, a stablecoin rail might be selected by the orchestration layer. On the other hand, if moving money cross-border in well traded currency pairs, using local schemes operated by players like Wise or Airwallex may be the better choice. Most legacy and local scheme operators are also exploring stablecoin options themselves to integrate an orchestration layer that allows smart routing across various rails. For these reasons, we believe that stablecoins will materially impact the world of cross-border payments.

The Evolving Market Landscape

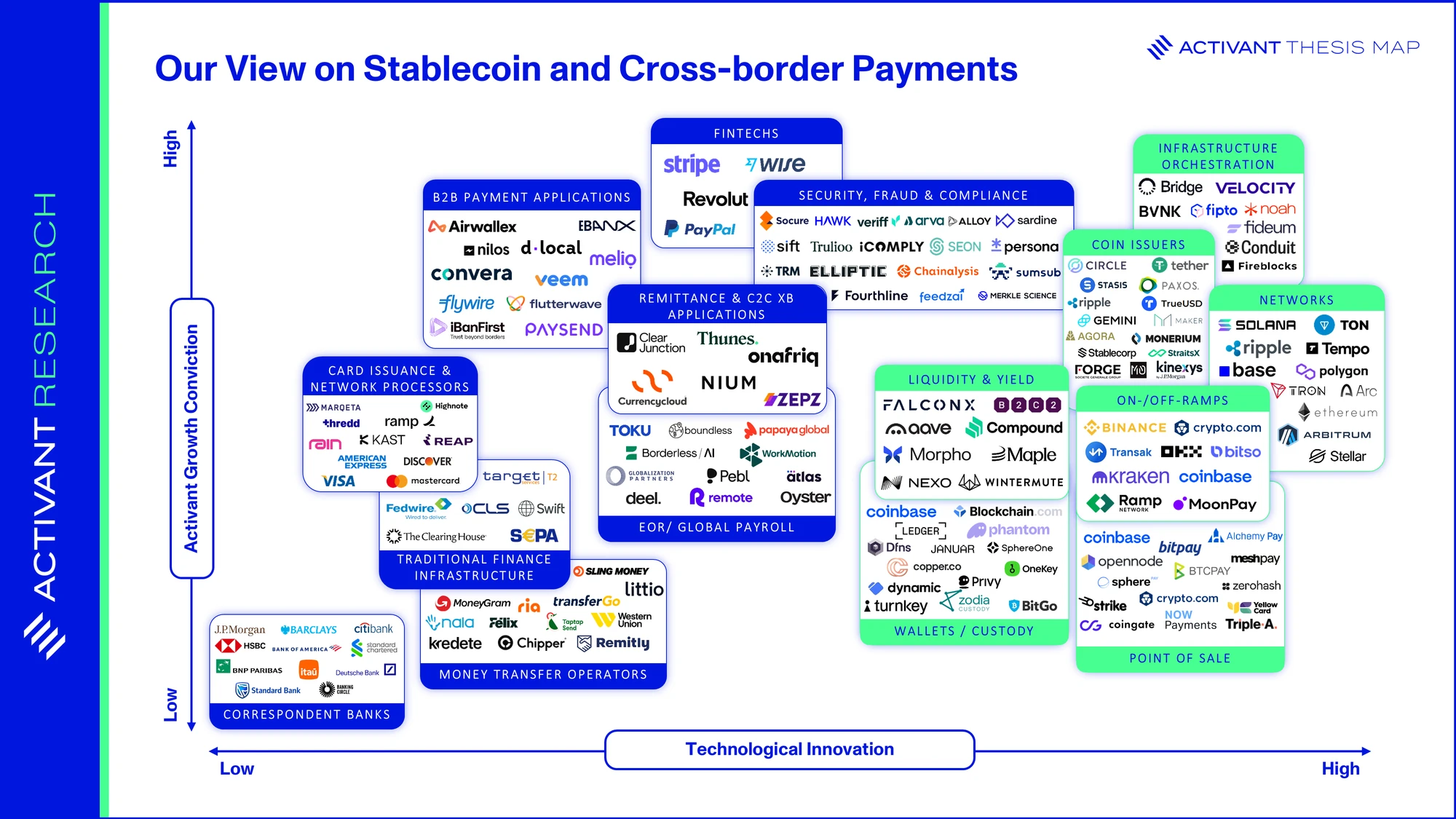

The battle to transform (or defend) international payments is being led by a diverse set of players – from entrenched banks and MTOs to crypto-native startups. To frame this complex ecosystem, we created an Activant Thesis Map that plots technological innovation against our view of segment growth. The categorization that follows reflects our best-effort assessment of where players operate today; we acknowledge that others may have a slightly different view.

Correspondent Banks: Institutions such as J.P. Morgan Chase, Citibank, HSBC and Deutsche Bank form the backbone of the current cross-border payments system and collectively handled ~92% of B2B cross-border volume in 2023.21 These banks are investing in improving their networks and exploring their own digital currencies. J.P. Morgan, for instance, created JPM Coin, a tokenized bank deposit used internally for instant wholesale payments.22 In Europe, Société Générale has launched its own stablecoin, CoinVertible, denominated in both dollars and euros.23

Card Issuance & Network Processors: Visa and Mastercard now both support settlement in stablecoins, positioning themselves as bridges between traditional payments and digital assets. By late 2025, Visa had processed approximately $3.5bn in stablecoin settlements, primarily using USDC on the Solana blockchain. Through its Tokenized Asset Platform, issuers and acquirers can settle obligations in USDC and link stablecoin wallets directly to card programs. Mastercard has taken a multi‑token approach, supporting several dollar‑ and euro‑denominated stablecoins and enabling seamless conversion between crypto and fiat.24

TraditionalFinance Infrastructure: SWIFT, the global messaging platform network underpinning correspondent banking, arguably has the most at stake and has begun developing blockchain‑based solutions to facilitate tokenized transactions between banks and to remain competitive with fintech and stablecoin‑native alternatives.

Money Transfer Operators (MTOs): Western Union, MoneyGram and Ria continue to play a critical role in remittances and consumer‑to‑consumer flows, particularly where cash remains dominant. Facing pressure from lower‑cost digital alternatives, they are increasingly integrating stablecoins into their offerings. MoneyGram’s partnership with the Stellar network, for example, enables customers to fund transfers in cash, convert to USDC, send value cross‑border, and cash out locally within minutes using its global agent network.25 Western Union is piloting similar initiatives, exploring wallet integrations and partnerships while also developing its own stablecoin.

Employer of Record (EOR) & Global Payroll Providers: Firms like Deel are exploring stablecoins to accelerate international salary payments, reduce FX friction and improve certainty around settlement timing. For globally distributed workforces and contractors paid across dozens of jurisdictions, stablecoins offer a potential way to simplify cross‑border payroll flows while reducing reliance on slow and opaque correspondent banking processes.

Remittance and C2C Cross-border Payments Applications: Platformssuch as Onafriq and Currencycloud provide critical connectivity across emerging‑market corridors, where stablecoins can meaningfully reduce costs and settlement times.

Stablecoin On-/Off-ramps: Exchanges like Coinbase and Binance, as well as fintech bridges that convert fiat to stablecoin and vice versa, are essential conduits for consumers to navigate the system and operate seamlessly between the fiat and stablecoin worlds. Many are now licensed as money transmitters or electronic money institutions. MoneyGram’s USDC cash service, for example, effectively acts as a physical on/off ramp in 170+ countries.26 Startups such as Bitso, a Mexican crypto exchange and unicorn, facilitate stablecoin and crypto remittances between the US and Latin America, handling billions in volume.

Stablecoin Liquidity & Yield Players: These firms play an increasingly important supporting role in the stablecoin ecosystem by supplying liquidity, balance-sheet efficiency, and yield opportunities that sit adjacent to payment flows. Players such as FalconX operate as digital-asset prime brokers, offering trading, financing and custody services that allow institutions to deploy and manage stablecoin liquidity at scale. Protocols such as Aave provide decentralized lending and borrowing infrastructure on networks like Ethereum, enabling stablecoin holders to earn yield or access short-term liquidity without relying on traditional intermediaries.

Stablecoin Issuers:These include a wave of crypto-native startups, serving as the lifeblood of the new rails. Tether and Circle, the two largest players that have issued about 88% of stablecoins in the market, are joined by a long and growing list of competitors.

Stablecoin Wallets & Custodians: These form the primary interface between users, institutions and stablecoin networks. Software wallets such as Phantom provide user-friendly access to blockchain networks, while hardware wallets like Ledger (an Activant portfolio company) prioritize security through offline key storage. However, as stablecoins move into mainstream enterprise use, self-custody models that require individuals to manage private keys are impractical and no organization will hand a single employee a secret key that controls access to corporate funds. Enterprises will require full custodial solutions that mirror the trust and governance structures of traditional banking, where a regulated partner manages key storage, access controls and transaction authorization on their behalf. Therefore, institutional custodians such as Copper are providing enterprise-grade custody, governance and risk controls, and the secure infrastructure required for businesses and financial institutions to hold and transact stablecoins at scale.

Stablecoin POS Players: These translate stablecoin functionality into practical merchant and enterprise use cases. Providers such as Singapore-based Triple-A enable businesses to accept stablecoins and cryptocurrencies while settling in fiat, with a particular focus on e-commerce and remittances. ZeroHash offers embedded crypto infrastructure — including trading, custody and settlement — that allows platforms to integrate stablecoin payments without building the stack in-house. Open-source provider BTCPay Server caters to merchants seeking direct, non-custodial crypto payment processing, highlighting the diversity of models emerging in this layer of the ecosystem.

Stablecoin/Blockchain Networks: Layer 1 and Layer 2 networks are building the foundation of decentralized payment networks. They offer the ledger that allows to on-/off-ramp, transfer and hold value in and across wallets.

Where Value Is Likely to Accrue

Our analysis indicates that a few segments and players are best positioned to benefit from the current shift away from legacy rails to faster and more cost-efficient rails. We are most excited about:

Stablecoin Infrastructure and Orchestration: These providers sit at the core of the ecosystem, helping to drive the growth of stablecoins. They enable easy adoption by seamlessly integrating and orchestrating various infrastructure components such as wallets and payment routing into customers’ existing payment, treasury and compliance systems. Fireblocks, for example, provides infrastructure to move, hold, manage and issue stablecoins. Its platform effectively acts as the operating system for stablecoin‑based payments and offers compliance by screening for AML risks, verifying wallet ownership, and automating Travel Rule compliance.Velocity is helping customers to optimize float through smart rail routing. UK-based BVNK similarly provides an enterprise platform for managed or self-managed stablecoin payments and reports handling ~$15 billion in annual volume.

Security, Fraud & Compliance Providers: These play a critical role as regulatory acceptance is a prerequisite for scale. Identity, fraud and compliance orchestration platforms such as Alloy, Sardine (an Activant portfolio company) and Socure sit primarily off‑chain, helping banks and fintechs onboard customers, verify identities, detect suspicious behavior, and manage KYC and AML workflows across fiat- and crypto‑enabled products. Alongside them, on‑chain analytics and RegTech providers focus on activity that occurs directly on public blockchains. Firms such as Chainalysis and Elliptic, together with specialists like TRM Labs, provide transaction tracing, wallet attribution, sanctions screening and risk scoring for stablecoin transfers.

Fintechs as Distribution and Trust Layers: By embedding stablecoins invisibly into familiar products, they drive user adoption and translate underlying technology into compelling customer experiences. Players like Wise (formerly TransferWise), Revolut, Stripe and PayPal have chipped away at the cross-border payments market and fee structure over the last decade. Wise built its $10+ billion business on the local scheme model that matches and nets local transfers to avoid cross-border fees, achieving dramatically lower costs. PayPal launched its own U.S. dollar stablecoin PYUSD in 2023, as did Stripe with USDB on their Bridge platform.27

B2B Payment Applications: These firms have started to apply stablecoins where they improve speed, cost or liquidity, offering an alternative rail that incrementally modernizes — rather than replaces — legacy cross‑border infrastructure. Players such as EBANX and Airwallex, which surpassed $1bn in annual recurring revenue in 2025, have started to experiment with stablecoin usage.28 They typically combine local accounts with stablecoin rails, offering corporates a pragmatic alternative rather than a wholesale replacement of existing systems.

Looking Ahead: What Customers Really Care About

What customers value is clear: low cost, high speed and transparency. They care about the experience, rather than the technology behind it — whether that’s correspondent banks, instant payment systems, or blockchains.

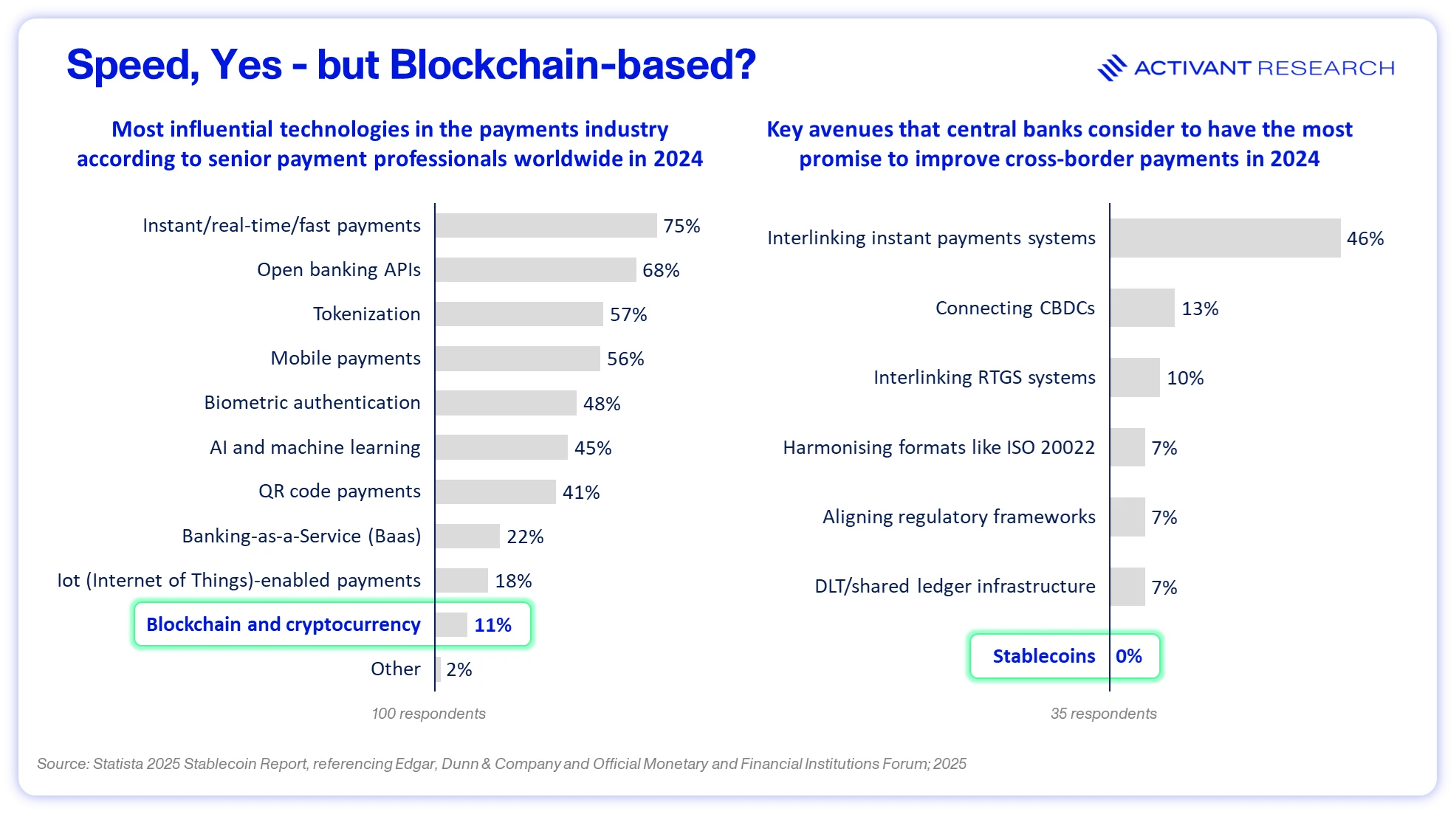

Stablecoins are not the only way of meeting these customer demands. While they are technologically impressive and operationally promising, they also introduce challenges, particularly around compliance, KYC and AML obligations. This ambivalence is reflected among industry professionals. Surveys of senior payments executives and central banks suggest that stablecoins are unlikely to become the dominant global payment rail.29

That said, in the medium-term stablecoins will continue to gain share and exert pressure on the high-cost legacy infrastructure of correspondent banking. Even limited adoption will challenge incumbent economics, forcing innovation and cost reduction. Their impact is likely to expand beyond payments: the liquidity and working capital benefits of near-instant settlement are compelling, and once enterprises experience those efficiencies firsthand, stablecoins will naturally extend into treasury management. Corporations will come for the payments but stay for the treasury benefits, as stablecoin wallets increasingly serve as the long-tail bank account for managing capital across complex currencies and jurisdictions where traditional banking infrastructure is slow, expensive or restrictive. Our optimistic perspective naturally depends on governments and regulators maintaining a broadly permissive stance rather than sharply restricting this new form of payment.

Over the longer term, stablecoins are unlikely to fully replace legacy systems. Instead, they are set to become an alternative rail within a multi-rail ecosystem, complementing increasingly interconnected and efficient instant payment and real-time gross settlement (RTGS) systems. While this may temper some of the more ambitious stablecoin narratives, it should not obscure the scale of the opportunity. Even a modest share of the more than $2 quadrillion in annual global payment flows is economically meaningful, positioning stablecoins as a durable and increasingly important component of the future payments landscape.

Footnotes

-

McKinsey & Company, 2025 Global Payments Report, September 2025 ↩

-

ibid ↩

-

McKinsey & Company, How banks can win back lower-value cross-border payments business, April 2025 ↩

-

The World Bank, Measuring the cost of cross-border B2B payments in the Balkans, August 2025 ↩

-

McKinsey & Company, How banks can win back lower-value cross-border payments business, April 2025 ↩

-

McKinsey & Company, The stable door opens: How tokenized cash enables next-gen payments, July 2025 ↩

-

Muyao Shen, Stablecoin sector may reach $2 trillion: Standard Chartered, Bloomberg, April 2025 ↩

-

McKinsey & Company, How banks can win back lower-value cross-border payments business, April 2025 ↩

-

FXCintelligence, The state of stablecoins in cross-border payments: The 2025 industry primer, July 2025 ↩

-

Chainalysis, The 2025 global adoption index, September 2025 ↩

-

McKinsey & Company, The stable door opens: How tokenized cash enables next-gen payments, July 2025 ↩

-

Boston Consulting Group, Stablecoins: Five killer tests to gauge their potential, May 2025 ↩

-

Ribbit Capital, Token Factory Letter, June 2025 ↩

-

ibid ↩

-

Token Terminal, Ethereum Average and Median Transaction Fees, January 13, 2026 ↩

-

Token Terminal, Arbitrum One Average and Median Transaction Fees, January 13, 2026 ↩

-

Token Terminal, L1 and L2 Blockchain technical performance, January 13, 2026 ↩

-

FXCIntelligence, Banking’s 2024 cross-border payments trends: A year in data, December 19, 2024 ↩

-

McKinsey & Company, The stable door opens: How tokenized cash enables next-gen payments, July 2025 ↩

-

Wellesley Hills Financial, Mechanics of Stablecoin Settlement on the Visa and Mastercard Networks, January 11, 2026 ↩

-

Forbes, MoneyGram partners with Ripple Competitor Stellar, April 2022 ↩

-

Forbes, MoneyGram partners with Ripple Competitor Stellar, April 2022 ↩

-

FXCintelligence, The state of stablecoins in cross-border payments: The 2025 industry primer, July 2025 ↩

-

Airwallex, Celebrating $1 billion in ARR, November 3, 2025 ↩

Disclaimer: The information contained herein is provided for informational purposes only and should not be construed as investment advice. The opinions, views, forecasts, performance, estimates, etc. expressed herein are subject to change without notice. Certain statements contained herein reflect the subjective views and opinions of Activant. Past performance is not indicative of future results. No representation is made that any investment will or is likely to achieve its objectives. All investments involve risk and may result in loss. This newsletter does not constitute an offer to sell or a solicitation of an offer to buy any security. Activant does not provide tax or legal advice and you are encouraged to seek the advice of a tax or legal professional regarding your individual circumstances.

This content may not under any circumstances be relied upon when making a decision to invest in any fund or investment, including those managed by Activant. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Activant. While taken from sources believed to be reliable, Activant has not independently verified such information and makes no representations about the current or enduring accuracy of the information or its appropriateness for a given situation.

Activant does not solicit or make its services available to the public. The content provided herein may include information regarding past and/or present portfolio companies or investments managed by Activant, its affiliates and/or personnel. References to specific companies are for illustrative purposes only and do not necessarily reflect Activant investments. It should not be assumed that investments made in the future will have similar characteristics. Please see "full list of investments" at activantcapital.com/companies/ for a full list of investments. Any portfolio companies discussed herein should not be assumed to have been profitable. Certain information herein constitutes "forward-looking statements." All forward-looking statements represent only the intent and belief of Activant as of the date such statements were made. None of Activant or any of its affiliates (i) assumes any responsibility for the accuracy and completeness of any forward-looking statements or (ii) undertakes any obligation to disseminate any updates or revisions to any forward-looking statement contained herein to reflect any change in their expectation with regard thereto or any change in events, conditions or circumstances on which any such statement is based. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking statements.